Hurst/VPIN Directional Strategy (Kraken Futures)

This is a Rust-only tutorial. The strategy, backtest wiring, and tests all live in the compiled core.

This tutorial backtests a directional strategy on PF_XBTUSD, the

USD-margined Bitcoin perpetual on Kraken Futures.

The strategy combines a Hurst-exponent regime filter with a VPIN

(Volume-synchronized Probability of Informed Trading) flow signal.

Historical trades and quotes come from Tardis.dev

and replay through the Rust BacktestEngine.

Introduction

The strategy combines three components: a slow regime filter derived from bars, a fast informed-flow signal derived from trades, and a quote-driven entry that fires only when both align.

-

Hurst exponent on dollar bars. Sampled on constant-notional (value) bars, following Lopez de Prado (Advances in Financial Machine Learning, Chapter 2). A rescaled-range (R/S) estimate above

0.55indicates persistent, trending behavior; below0.50the series is mean-reverting or noise. -

VPIN from trade aggressor flow. Each completed dollar bar is treated as one volume bucket. The absolute imbalance between aggressive buy and aggressive sell volume, averaged over the last fifty buckets, gives the VPIN level. The signed imbalance gives the net informed direction.

-

Quote-driven entry. Once both signals agree, the strategy opens a position on the next quote tick. Entry timing stays tied to the live top of book rather than to bar closes.

Exit is driven by the same ingredients: position is closed when the Hurst estimate decays back through a lower threshold, or when a holding-time cap is reached.

The strategy is shipped as

HurstVpinDirectional

in the nautilus_trading::examples::strategies module. As with all

shipped example strategies, it is intentionally simple and has no alpha

advantage.

Why Kraken Futures

Kraken Futures lists perpetuals on Bitcoin and Ether in two forms:

PI_inverse perpetuals: quoted in USD, margined and settled in the underlying.PF_linear perpetuals: quoted in USD, margined and settled in USD (via multi-collateral).

The tutorial uses PF_XBTUSD so the account currency, quote

currency, and dollar-bar sampling frame are all USD.

Why dollar bars and VPIN together

VPIN is defined on volume buckets rather than time buckets. Dollar

bars (VALUE aggregation in NautilusTrader) close after a fixed

notional has traded, so the sampling frame adapts to market activity.

Defining each VPIN bucket as one dollar bar keeps both signals on the

same clock, and Hurst sampled on the same bars uses the same frame.

Prerequisites

- A working Rust toolchain (see rustup.rs).

- The NautilusTrader repository cloned and building.

- Internet access to download a free Tardis sample (no API key required for the first day of each month).

Data preparation

Kraken Futures is published by Tardis under the historical slug

cryptofacilities. The first day of each month is available for free

without an API key, which is enough for a single-day plumbing check. A

full backtest needs at least two sessions to warm the 128-bar Hurst

window, which requires a paid Tardis API key (see the tip below).

mkdir -p /tmp/tardis_kraken

curl -L -o /tmp/tardis_kraken/PF_XBTUSD_trades.csv.gz \

https://datasets.tardis.dev/v1/cryptofacilities/trades/2024/01/01/PF_XBTUSD.csv.gz

curl -L -o /tmp/tardis_kraken/PF_XBTUSD_quotes.csv.gz \

https://datasets.tardis.dev/v1/cryptofacilities/quotes/2024/01/01/PF_XBTUSD.csv.gzThe runnable example binary shown later in this tutorial reads from

/tmp/tardis_kraken/ by default, so downloading into that directory up front

means cargo run works without needing KRAKEN_TRADES or KRAKEN_QUOTES

overrides.

Full historical ranges require a paid Tardis API key. Use the Tardis download utility for bulk fetches once you move beyond single-day samples.

The Rust Tardis loader parses .csv.gz directly and tags each record

with the instrument ID we supply, so no symbology mapping is needed at

the strategy level:

use nautilus_model::identifiers::InstrumentId;

use nautilus_tardis::csv::load::{load_quotes, load_trades};

let instrument_id = InstrumentId::from("PF_XBTUSD.KRAKEN");

let trades = load_trades(

"PF_XBTUSD_trades.csv.gz",

Some(1), // price_precision

Some(4), // size_precision

Some(instrument_id),

None, // limit

)?;

let quotes = load_quotes(

"PF_XBTUSD_quotes.csv.gz",

Some(1),

Some(4),

Some(instrument_id),

None,

)?;Pass the instrument's price_precision and size_precision explicitly. The

loader otherwise infers precision from the first few records, and a sample

day without fractional prices can infer 0, which the matching engine will

reject when it sees a quote tick that does not match the instrument's

declared precision.

Instrument definition

Since we are loading CSV data directly rather than through the live

Kraken adapter, we define PF_XBTUSD manually as a

CryptoPerpetual.

Linear perpetuals on Kraken Futures are quoted and margined in USD:

use nautilus_model::{

identifiers::{InstrumentId, Symbol},

instruments::CryptoPerpetual,

types::{Currency, Price, Quantity},

};

use rust_decimal_macros::dec;

let instrument = CryptoPerpetual::builder()

.instrument_id(InstrumentId::from("PF_XBTUSD.KRAKEN"))

.raw_symbol(Symbol::from("PF_XBTUSD"))

.base_currency(Currency::BTC()) // base

.quote_currency(Currency::USD()) // quote

.settlement_currency(Currency::USD()) // settlement (linear)

.is_inverse(false)

.price_precision(1)

.size_precision(4)

.price_increment(Price::from("0.5"))

.size_increment(Quantity::from("0.0001"))

.margin_init(dec!(0.02))

.margin_maint(dec!(0.01))

.maker_fee(dec!(0.0002))

.taker_fee(dec!(0.0005))

.ts_event(0.into())

.ts_init(0.into())

.build()

.unwrap();Fees and margin are explicit backtest assumptions. Check the Kraken Futures fee schedule for current rates.

Dollar-bar sampling

NautilusTrader ships all the information-driven bar aggregators from

AFML Chapter 2: tick, volume, value (dollar), plus imbalance and runs

variants for each. We use plain VALUE bars here, which close after a

fixed notional has traded on the tape.

The bar type is expressed as a string. The INTERNAL suffix tells the

engine to aggregate inside NautilusTrader from the underlying trade

stream (price type LAST):

use nautilus_model::data::BarType;

let bar_type = BarType::from("PF_XBTUSD.KRAKEN-2000000-VALUE-LAST-INTERNAL");Each bar closes after USD 2,000,000 of traded notional. A session

typically prints under 150 bars at this size, short of the 128-bar Hurst

window, so warming the defaults needs multiple sessions. For a single-day

run, either shrink the bar size to USD 500,000 or drop hurst_window

and vpin_window accordingly. Full multi-day backtests should use the

defaults.

VALUE bars are a view onto the trade tape. The backtest engine

consumes the same stream that drives VPIN, so there is no double

counting.

Strategy overview

The HurstVpinDirectional strategy runs three concurrent pipelines that

synchronize at bar close: trades feed a bucket accumulator, bar close

triggers signal recomputation, and quotes drive entry and timeout

checks.

- Per trade: accumulate aggressive buy and aggressive sell volume

for the current dollar-bar bucket using

TradeTick::aggressor_side. - Per bar (bucket close): append the bar's log return to the Hurst

window, compute the bucket's signed and absolute imbalance, reset

the accumulators, re-estimate rolling Hurst and VPIN, clear

exit_cooldown, and check regime exit. - Per quote: if flat and both signals agree (Hurst trending, VPIN above threshold, signed imbalance non-zero), open a market IOC order. If already positioned, check the holding-time cap.

Regime exit fires from the bar pipeline when Hurst drops below

hurst_exit. Holding timeout fires from the quote pipeline when the

position has been open longer than max_holding_secs.

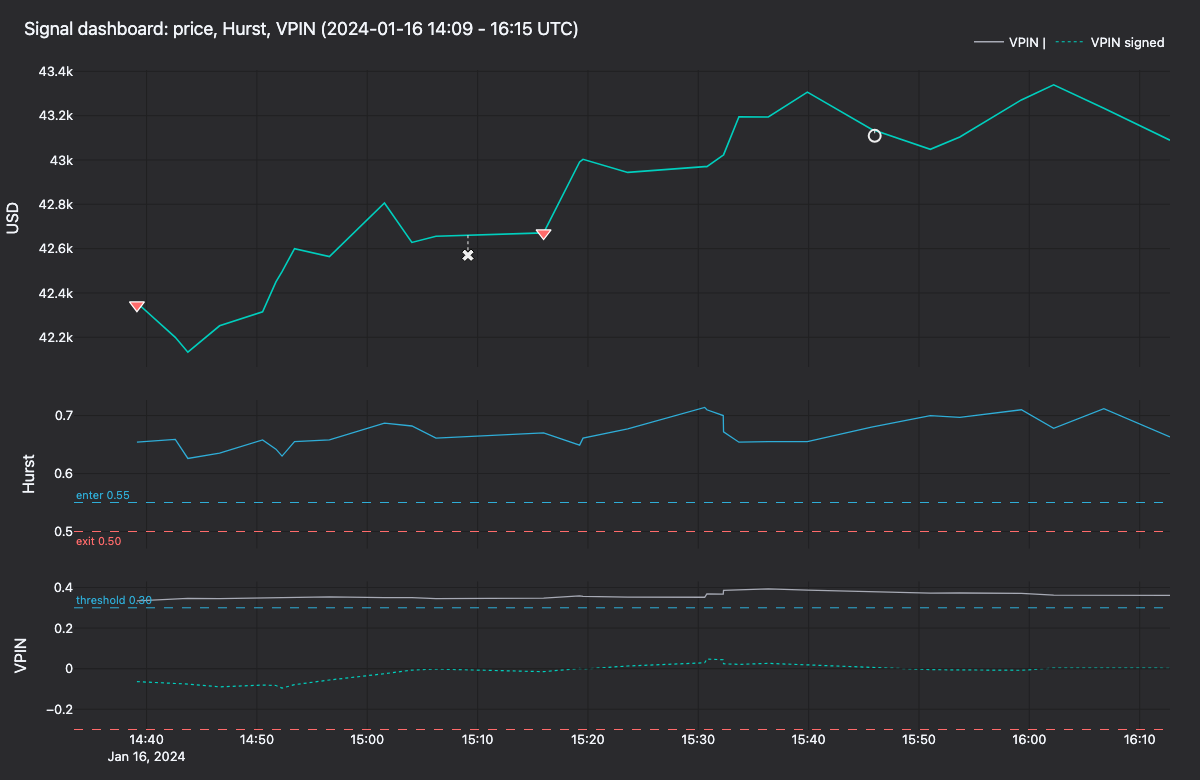

Figure 1. Signal dashboard for 2024-01-16 14:09-16 UTC: close, Hurst, VPIN. Markers sit at actual fill price; dotted connector shows slip against the bar-close line.

Hurst estimator

The strategy uses classical rescaled-range (R/S) regression. For each

lag k in (4, 8, 16, 32), the return window

is split into non-overlapping chunks of length k, each chunk's

rescaled range is computed, and the mean R/S is recorded. The slope of

log(R/S) vs log(k) across the lag set gives the Hurst estimate.

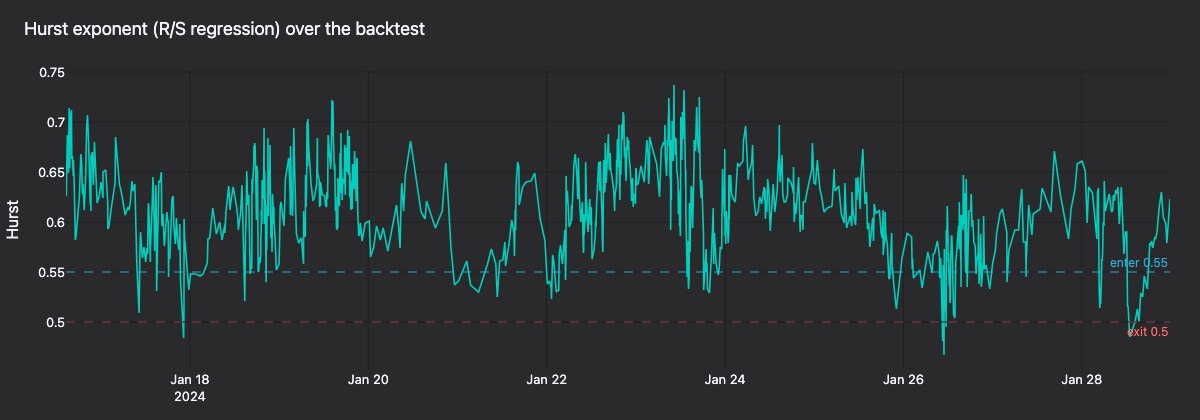

Figure 2. Rolling Hurst across 14 days of PF_XBTUSD (2024-01-15 to 2024-01-28) with enter 0.55 and exit 0.50 thresholds.

VPIN estimator

With explicit trade aggressor side available from the venue feed, VPIN collapses to

VPIN = mean_k ( |V_B_k - V_S_k| / (V_B_k + V_S_k) )over the last k completed dollar-bar buckets. The signed variant

retains the sign of V_B - V_S and is used to choose direction. This

is more accurate than the bulk-volume classification used in the

original Easley/Lopez de Prado formulation, which was only necessary

when aggressor side was not directly observable.

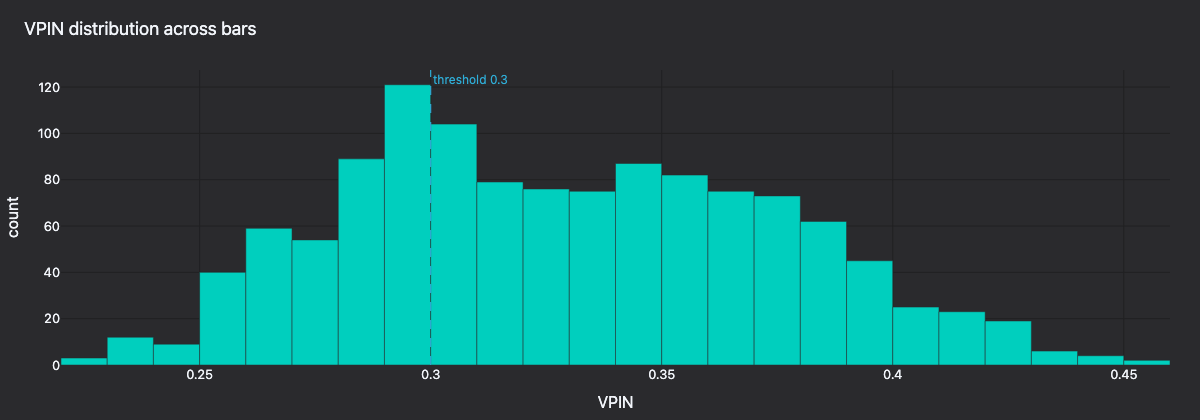

Figure 3. VPIN distribution across all bars with the 0.30 entry threshold.

Configuration

| Parameter | Value | Description |

|---|---|---|

bar_type | 2M-VALUE-LAST | Dollar bars closing every USD 2,000,000 of notional. |

trade_size | 0.0100 | 0.0100 XBT per trade (matches instrument precision). |

hurst_window | 128 | Rolling window of dollar bar log returns. |

hurst_lags | [4, 8, 16, 32] | Lag set used in the R/S regression. |

hurst_enter | 0.55 | Above this, the regime is treated as trending. |

hurst_exit | 0.50 | Below this, open positions are flattened. |

vpin_window | 50 | Completed volume buckets averaged for VPIN. |

vpin_threshold | 0.30 | Minimum VPIN for flow to be considered informed. |

max_holding_secs | 1800 | Seconds a position may be held (default 3600; overridden here). |

Dollar-bar size, Hurst lags, and VPIN window are all coupled. Smaller bars give faster reaction but noisier Hurst; larger bars smooth both signals but risk too few samples in a single-day backtest.

Backtest setup

Configure a BacktestEngine with a Kraken venue and a USD starting balance:

use nautilus_backtest::{

config::{BacktestEngineConfig, SimulatedVenueConfig},

engine::BacktestEngine,

};

use nautilus_model::{

data::Data,

enums::{AccountType, BookType, OmsType},

identifiers::Venue,

instruments::{Instrument, InstrumentAny},

types::Money,

};

let mut engine = BacktestEngine::new(BacktestEngineConfig::default())?;

engine.add_venue(

SimulatedVenueConfig::builder()

.venue(Venue::from("KRAKEN"))

.oms_type(OmsType::Netting)

.account_type(AccountType::Margin)

.book_type(BookType::L1_MBP)

.starting_balances(vec![Money::from("100_000 USD")])

.build()?,

)?;

engine.add_instrument(&InstrumentAny::CryptoPerpetual(instrument))?;Feed the loaded trades and quotes as Data enum variants:

let mut data: Vec<Data> = trades.into_iter().map(Data::Trade).collect();

data.extend(quotes.into_iter().map(Data::Quote));

engine.add_data(data, None, true, true)?;Add the strategy

use nautilus_model::types::Quantity;

use nautilus_trading::examples::strategies::{

HurstVpinDirectional, HurstVpinDirectionalConfig,

};

let config = HurstVpinDirectionalConfig::builder()

.instrument_id(instrument_id)

.bar_type(bar_type)

.trade_size(Quantity::from("0.0100")) // match instrument size_precision

.max_holding_secs(1800)

.build();

engine.add_strategy(HurstVpinDirectional::new(config))?;Run the backtest

engine.run(None, None, None, false)?;With the default 128/50 windows and USD 2,000,000 bars, a single-day sample stays in warmup for the whole run. The run will show the engine aggregating dollar bars and driving the strategy at trade and quote granularity, but Hurst and VPIN will not emit until the windows are full. To see signal updates and entry/exit logic fire on a single day, shrink the bar size or windows as noted above, or provide two or more sessions of data.

A 14-day run (2024-01-15 to 2024-01-28) on this configuration prints

1,224 bars and fires only 2 entries, 1 partial cover, and 1 close.

Entries are sparse by design: both hurst_enter and vpin_threshold

must clear on the same quote. The residual size after the partial IOC

cover stays open through the rest of the session, which is how a Netting

OMS resolves an exit IOC that only fills part of the resting position.

The wiring above is shipped as a runnable binary:

cargo run -p nautilus-kraken --features examples \

--example kraken-hurst-vpin-backtest --releaseBy default it reads PF_XBTUSD_trades.csv.gz and PF_XBTUSD_quotes.csv.gz

from /tmp/tardis_kraken/. Override with KRAKEN_TRADES and

KRAKEN_QUOTES environment variables.

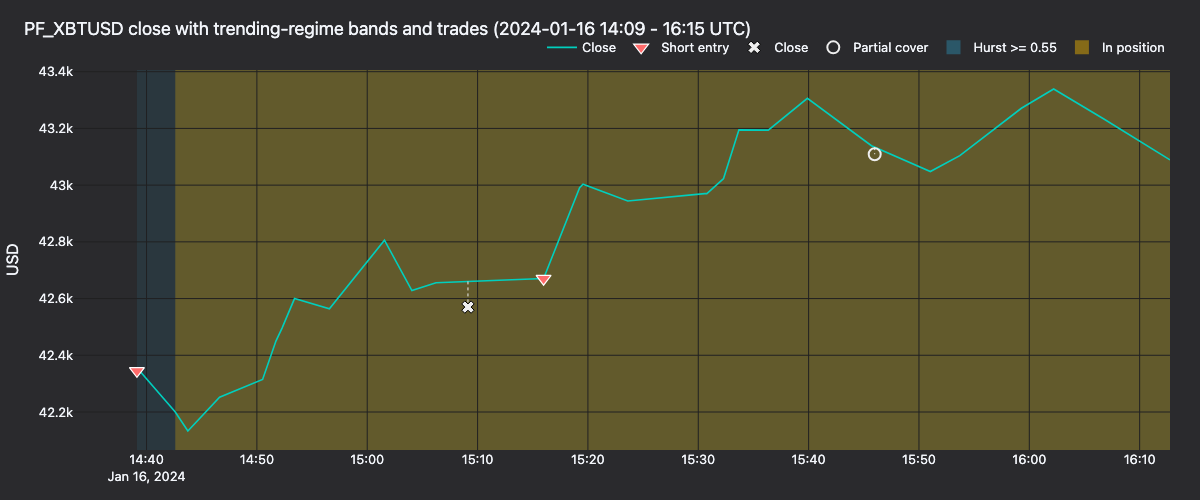

Figure 4. Close price for 2024-01-16 14:09-16 UTC. Teal bands mark

Hurst >= 0.55 bars; gold bands mark periods with an open position. Markers

sit at actual fill price; dotted connector shows slip against the bar-close

line.

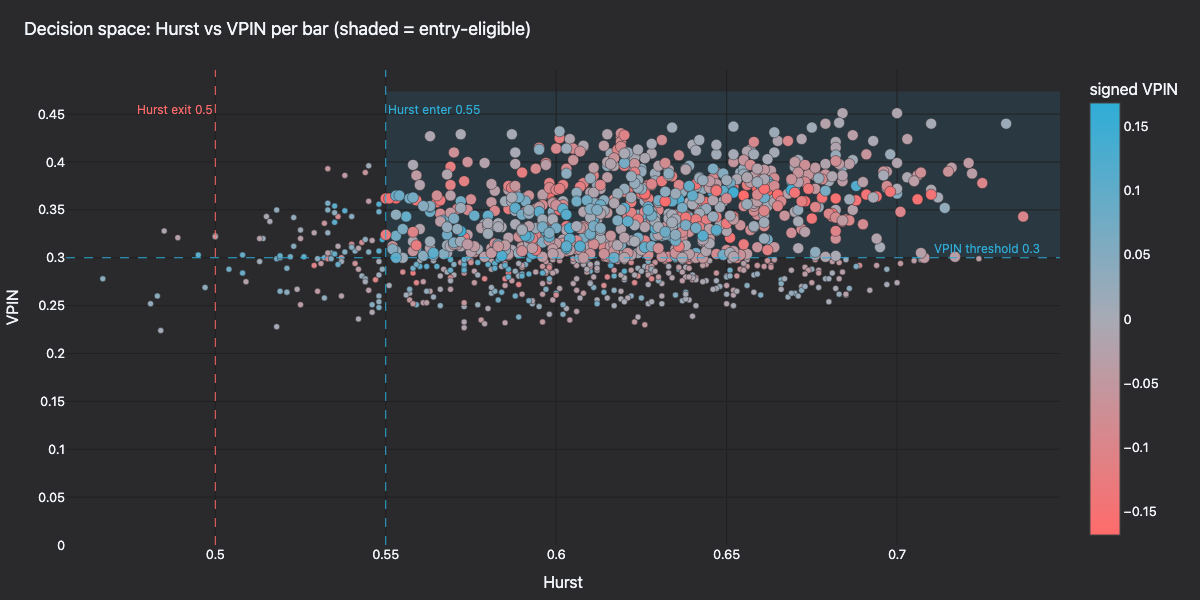

Figure 5. Per-bar Hurst vs. VPIN across the backtest, colored by signed VPIN. Shaded quadrant marks the entry-eligible region.

Regenerate the panels

The backtest strategy logs Hurst=… VPIN=… signed=… bar_close=… on every

bar close and standard OrderFilled events on entries and exits, so the

panels above are fully reproducible from the run's stdout:

RUST_LOG=info cargo run -p nautilus-kraken --features examples \

--example kraken-hurst-vpin-backtest --release > /tmp/backtest.log 2>&1

uv sync --extra visualization

BACKTEST_LOG=/tmp/backtest.log \

python3 docs/tutorials/assets/hurst_vpin_kraken/render_panels.pyThe renderer uses the shared nautilus_dark tearsheet theme and writes

static PNGs via Plotly's Kaleido exporter.

Next steps

-

Tune the sampling frame. Try larger or smaller dollar-bar thresholds. The

VALUE_IMBALANCEandVALUE_RUNSaggregators produce bars that close on information arrival itself, which may be an interesting substitute for constant-dollar sampling. -

Tighten the thresholds.

hurst_enter,hurst_exit, andvpin_thresholdall interact: a higher enter threshold makes signals rarer but more specific; a tighter exit shortens average holding time. -

Add a volatility gate. Overlay a realized-volatility estimator on the same bars to suppress entries during clearly chaotic sessions.

-

Go live on Kraken Futures demo. Once the backtest behaves, drive the same strategy through the Kraken live client factories against demo-futures.kraken.com. A runnable live wiring ships as:

cargo run -p nautilus-kraken --features examples \ --example kraken-hurst-vpin-liveSet

KRAKEN_FUTURES_API_KEYandKRAKEN_FUTURES_API_SECRETin the environment before running.

Further reading

HurstVpinDirectionalstrategy source- Data concepts: bar types and aggregation

- Tardis integration guide

- Kraken integration guide

- Kraken Futures documentation

- Lopez de Prado, M. (2018). Advances in Financial Machine Learning, Wiley. Chapter 2 (information-driven bars) and Chapter 19 (VPIN).

Composite Market Making on Lighter RWA with Databento US Equities NVDA

This tutorial runs the shipped [CompositeMarketMaker][composite-market-maker] strategy on Lighter's NVDA-PERP.LIGHTER RWA market using Databento NVDA.EQUS...

Integrations

NautilusTrader uses modular adapters to connect to trading venues and data providers, translating raw APIs into a unified interface and normalized domain model.