Composite Market Making on Lighter RWA with Databento US Equities NVDA

This tutorial runs the shipped CompositeMarketMaker strategy on Lighter's

NVDA-PERP.LIGHTER RWA market using Databento NVDA.EQUS quotes as an external

signal. The strategy quotes one post-only bid and one post-only ask around the

Lighter mid, then shifts both sides from a normalized Databento residual and the

current Lighter inventory.

The setup uses a Rust LiveNode, while the strategy itself runs as the native

Rust CompositeMarketMaker strategy. If you are new to the Lighter adapter, start with

Get started with Lighter first. That guide isolates the Rust and Python v2

data-client paths before this tutorial adds Databento signal data and live order flow.

Introduction

Lighter lists real-world asset (RWA) perpetuals that trade continuously, including

single-name equity markets. See Lighter's RWA docs and market specifications

for current venue details. Databento's US Equities

datasets provide US equity top-of-book data for NVDA, with mbp-1 available

through the Nautilus Databento adapter.

CompositeMarketMaker is a small two-input market maker:

- The target instrument is the Lighter market to quote:

NVDA-PERP.LIGHTER. - The signal instrument is the Databento reference feed:

NVDA.EQUS. - The anchor is the Lighter mid.

- The signal residual is

(databento_mid / baseline) - 1.0. - The quote shift is

signal_skew_factor * residual - inventory_skew_factor * net_position.

With no configured baseline, the strategy captures the first observed NVDA.EQUS

mid as the reference price. The residual starts at zero and measures NVDA's move

from that first signal mid, not the Lighter/Databento basis. Set the

SIGNAL_BASELINE constant in the example source to pin the reference price for

deterministic runs.

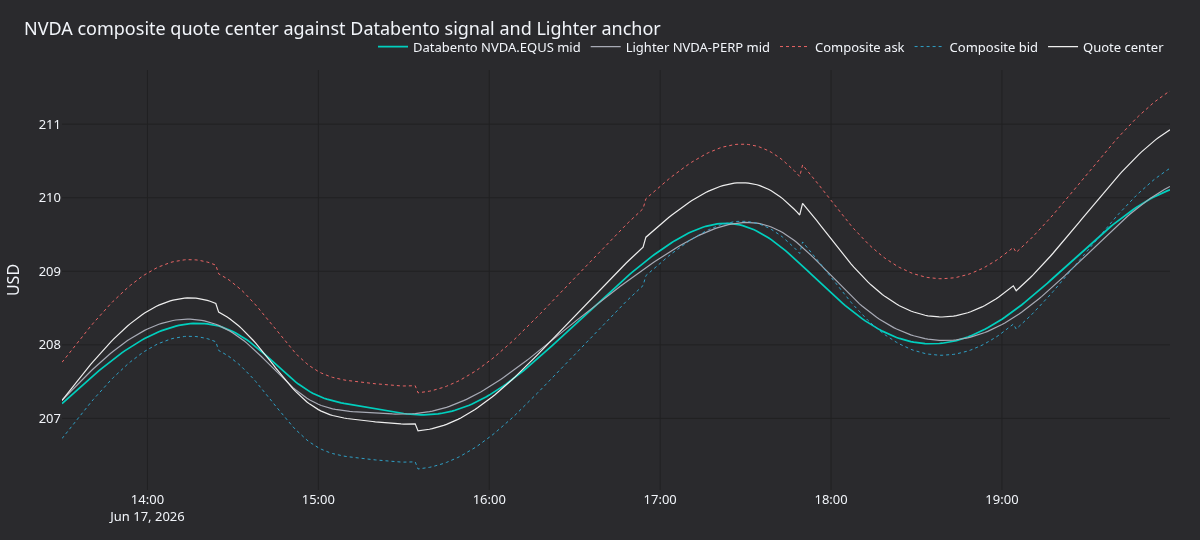

In this setup, the Lighter BBO remains the spread anchor. Databento moves the quote center up or down through the normalized residual.

The focus is the adapter wiring: one engine consumes a direct US equity feed and a crypto-native RWA venue, while order lifecycle, inventory, and quote state stay inside the same event-driven runtime.

Prerequisites

- A Rust toolchain (MSRV 1.97.1 or newer).

- A Cargo project with the Nautilus, Lighter, and Databento crates as dependencies (see Project setup).

- Python 3.12+ to regenerate the rendered panels.

- A Databento API key with live access to Databento US Equities Mini

(

EQUS.MINI), the default dataset for the bundledNVDA.EQUSroute. Higher tiers such asEQUS.PLUSneed a separate Databento license; select one withvenue_dataset_mapwhen your account is entitled. - Lighter API credentials (numeric account index, API key index, and API secret) for the configured environment (testnet by default), required only to connect and submit orders.

- The Lighter integration guide: Lighter.

- The Databento integration guide: Databento.

The example reads credentials from environment variables and keeps the strategy

parameters as editable Rust constants. It defaults to

LighterEnvironment::Testnet, so set the testnet Lighter credentials:

export DATABENTO_API_KEY="your-databento-api-key"

export LIGHTER_TESTNET_ACCOUNT_INDEX="123456"

export LIGHTER_TESTNET_API_KEY_INDEX="0"

export LIGHTER_TESTNET_API_SECRET="your-lighter-api-secret"For mainnet, change LIGHTER_ENVIRONMENT in the source to

LighterEnvironment::Mainnet and use the mainnet LIGHTER_* credential

variables described in the integration guide. Set DATABENTO_API_KEY before

running the example.

Project setup

The strategy, node, and adapters ship as crates, so you can depend on them from

your own Cargo project rather than working inside a NautilusTrader checkout. Add

the following to your Cargo.toml, pointing every Nautilus dependency at the

same develop git source so the crates resolve to one consistent version:

[dependencies]

nautilus-common = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["live"] }

nautilus-core = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop" }

nautilus-databento = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["high-precision", "live"] }

nautilus-lighter = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["examples", "high-precision"] }

nautilus-live = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["node"] }

nautilus-model = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["high-precision"] }

nautilus-trading = { git = "https://github.com/nautechsystems/nautilus_trader.git", branch = "develop", features = ["examples", "high-precision"] }

tokio = { version = "1", features = ["full"] }The examples feature on nautilus-trading exposes the CompositeMarketMaker

strategy, and high-precision is required for Lighter's crypto-native pricing.

For the general crate layout, feature flags, and the crates.io alternative to

the git source, see the Rust project setup guide.

The Databento client also needs a publishers file that maps venues to datasets.

Download publishers.json from the Databento adapter

crate and point publishers_filepath at your local copy. The shipped example

resolves the same file relative to the checkout, so this step only applies to

your own project.

Why NVDA

NVDA is a liquid Nasdaq-listed single-name equity, and Lighter maps its RWA

perpetual to NVDA-PERP.LIGHTER. This pairs a licensed Databento signal with a

Lighter traded market:

| Role | Instrument ID | Source | Notes |

|---|---|---|---|

| Signal instrument | NVDA.EQUS | Databento | EQUS.MINI top‑of‑book quote updates. |

| Target instrument | NVDA-PERP.LIGHTER | Lighter | RWA perpetual traded through Lighter. |

Subscribing to NVDA.EQUS requests top-of-book (mbp-1) quotes for NVDA from

Databento's EQUS.MINI dataset by default, delivered as a single QuoteTick

stream. EQUS.MINI is the lowest-cost consolidated US equities tier; richer

tiers such as EQUS.PLUS need a separate Databento license and can be selected

with the client's venue_dataset_map (for example {"EQUS": "EQUS.PLUS"}) once

your account is entitled. The adapter resolves the EQUS venue from a publishers

file: the example points DatabentoLiveClientConfig at the publishers.json

bundled with the Databento adapter. See Instrument IDs and symbology

for the mapping rules.

The older Databento Equities Basic (DBEQ.BASIC) dataset name appears in some

grandfathered accounts and historical examples. New Databento subscriptions use

the Databento US Equities product line, so this tutorial uses the consolidated

EQUS venue. Treat the top-of-book feed as a licensed signal proxy for the

tutorial wiring, not as a full depth Nasdaq TotalView book.

The example starts at trade_size=0.05, which aligns with the Lighter NVDA

minimum base amount observed during tutorial validation. Check the

market details endpoint before increasing size or changing instruments.

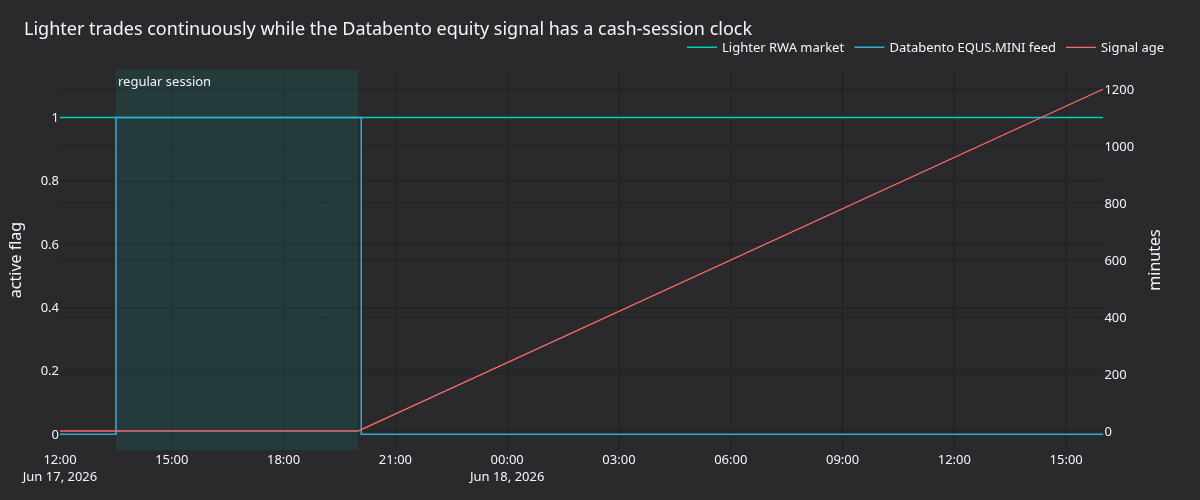

Session constraint

Lighter RWA markets trade continuously. NVDA.EQUS follows the US equity market

data session. The first live test should run during the regular cash session

(13:30-20

CompositeMarketMaker does not include a built-in session gate or signal-age

guard. For production use, add an actor or strategy variant that cancels quotes

when the Databento signal goes stale. The tutorial example keeps this explicit

instead of hiding it in a custom strategy.

Example node

There are two ways to run this: from a NautilusTrader checkout via the shipped

Lighter NVDA composite market maker example binary, or by

copying the node wiring below into a main in your own project that depends on

the crates from Project setup. A Python v2 counterpart also lives at

python/examples/lighter/nvda_composite_mm.py; it uses the same Rust

strategy through PyO3.

From a checkout, with the credential variables set, the shipped binary connects

the data and execution clients. It defaults to DRY_RUN = true, which starts

the clients without adding the order-submitting strategy:

cargo run --bin lighter-nvda-composite-mm --package nautilus-tutorials --features examplesDatabento is a multi-venue data client without a fixed venue route, so the engine

uses it as the default route for NVDA.EQUS. Lighter registers with the LIGHTER

venue route and receives NVDA-PERP.LIGHTER subscriptions.

The core of the setup is the three-client node plus CompositeMarketMaker:

let lighter_environment = LIGHTER_ENVIRONMENT;

let trader_id = TraderId::from(TRADER_ID);

let account_id = AccountId::from(ACCOUNT_ID);

let instrument_id = InstrumentId::from(INSTRUMENT_ID);

let signal_instrument_id = InstrumentId::from(SIGNAL_INSTRUMENT_ID);

let databento_api_key = get_env_var("DATABENTO_API_KEY")?;

let databento_config =

DatabentoLiveClientConfig::new(databento_api_key, publishers_filepath, true, true);

let lighter_data_config = LighterDataClientConfig::builder()

.environment(lighter_environment)

.build();

let lighter_exec_config = LighterExecClientConfig::builder()

.trader_id(trader_id)

.account_id(account_id)

.environment(lighter_environment)

.build();

let mut strategy_config = CompositeMarketMakerConfig::builder()

.instrument_id(instrument_id)

.signal_instrument_id(signal_instrument_id)

.max_position(max_position)

.trade_size(trade_size)

.half_spread_bps(HALF_SPREAD_BPS)

.inventory_skew_factor(INVENTORY_SKEW_FACTOR)

.signal_skew_factor(SIGNAL_SKEW_FACTOR)

.requote_threshold_bps(REQUOTE_THRESHOLD_BPS)

.on_cancel_resubmit(ON_CANCEL_RESUBMIT)

.build();

strategy_config.base.strategy_id = Some(StrategyId::from("NVDA_COMPOSITE_MM-001"));

strategy_config.base.order_id_tag = Some("001".to_string());

let mut node = LiveNode::builder(trader_id, Environment::Live)?

.with_name("LIGHTER-NVDA-COMPOSITE-MM-001".to_string())

.with_reconciliation(!DRY_RUN)

.add_data_client(

None,

Box::new(DatabentoDataClientFactory::new()),

Box::new(databento_config),

)?

.add_data_client(

None,

Box::new(LighterDataClientFactory::new()),

Box::new(lighter_data_config),

)?

.add_exec_client(

None,

Box::new(LighterExecutionClientFactory::new()),

Box::new(lighter_exec_config),

)?

.build()?;

if !DRY_RUN {

node.add_strategy(CompositeMarketMaker::new(strategy_config))?;

}To allow order submission, edit the constant near the top of the example source:

const DRY_RUN: bool = false;Then run the same command:

cargo run --bin lighter-nvda-composite-mm --package nautilus-tutorials --features examplesThis command can submit live orders when DRY_RUN is false. Start with the smallest accepted size

on a funded test account or a mainnet account sized for loss. Confirm the active instrument ID,

account ID, numeric account index, and Lighter credentials before changing it.

For a testnet smoke run, keep LIGHTER_ENVIRONMENT as

LighterEnvironment::Testnet and use the LIGHTER_TESTNET_* credential

variables. If the run is outside the Databento US Equities cash session, it can

still validate node startup, routing, Lighter data, and the order lifecycle. The

Databento residual remains zero until the first NVDA.EQUS quote arrives.

Strategy parameters

| Parameter | Value | Description |

|---|---|---|

instrument_id | NVDA-PERP.LIGHTER | Lighter RWA perpetual to quote. |

signal_instrument_id | NVDA.EQUS | Databento US Equities Mini signal feed. |

trade_size | 0.05 | Size per bid or ask. |

max_position | 0.20 | Hard cap on net Lighter exposure. |

half_spread_bps | 25 | Half‑spread around the Lighter anchor. |

inventory_skew_factor | 2.0 | Price units per unit of net position. |

signal_skew_factor | 55.0 | Price units per unit of normalized Databento residual. |

signal_baseline | First signal mid | Optional reference price for the Databento residual. |

requote_threshold_bps | 5 | Anchor or signal‑impact move that triggers cancel and requote. |

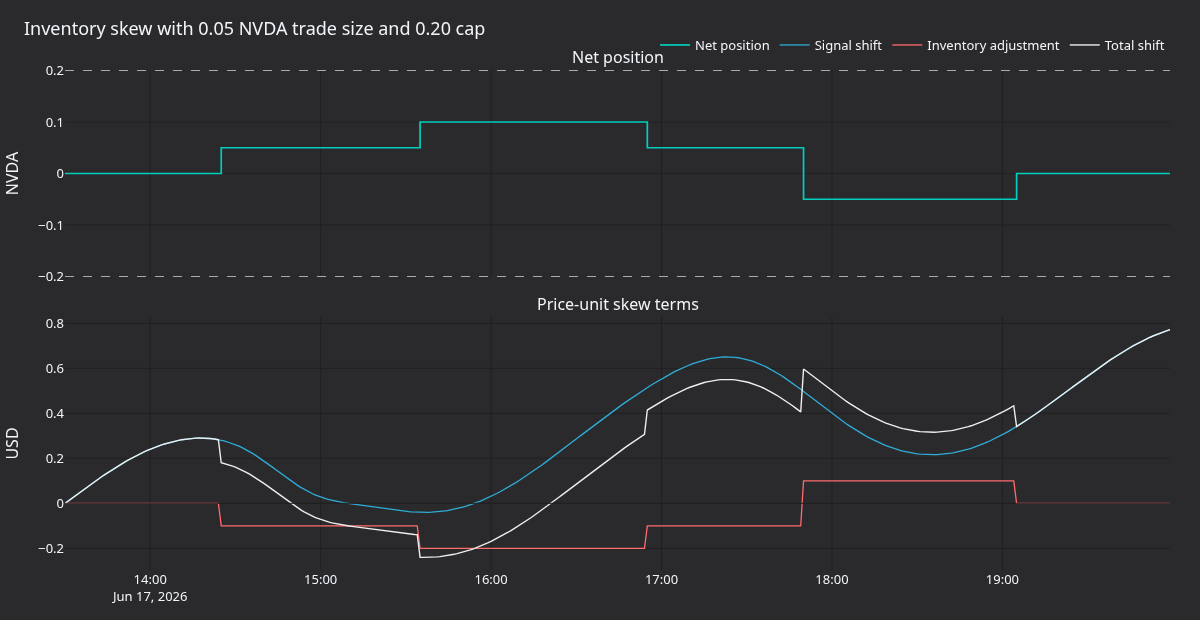

With a Lighter mid of 207.00 and half_spread_bps=25, the unskewed half

spread is 0.5175 USD. If Databento is 30 bps above its baseline, a

signal_skew_factor of 55.0 shifts both sides up by 0.165 USD before

inventory skew. A long position of 0.05 with inventory_skew_factor=2.0

shifts both sides down by 0.10 USD.

Requote behavior

Signal ticks update internal state but do not submit orders by themselves. Until the first Databento quote arrives, the residual is zero. The next Lighter quote tick reads the latest signal residual and checks the quote state. A quote cycle occurs when:

- no target orders are open or in-flight;

- the Lighter anchor moves by at least

requote_threshold_bps; or - the price impact of the signal residual change clears the same threshold.

The strategy then cancels open orders, reads current net position and pending

exposure from the cache, computes one bid and one ask, drops any side that

breaches max_position, and submits the remaining sides as post-only limits.

Panels

The panels below use deterministic replay data. They show the quoting mechanics and the cash-session constraint. They are not a captured live Lighter fill trace.

Figure 1. Databento NVDA.EQUS mid, Lighter NVDA-PERP.LIGHTER mid,

composite bid, composite ask, and quote center.

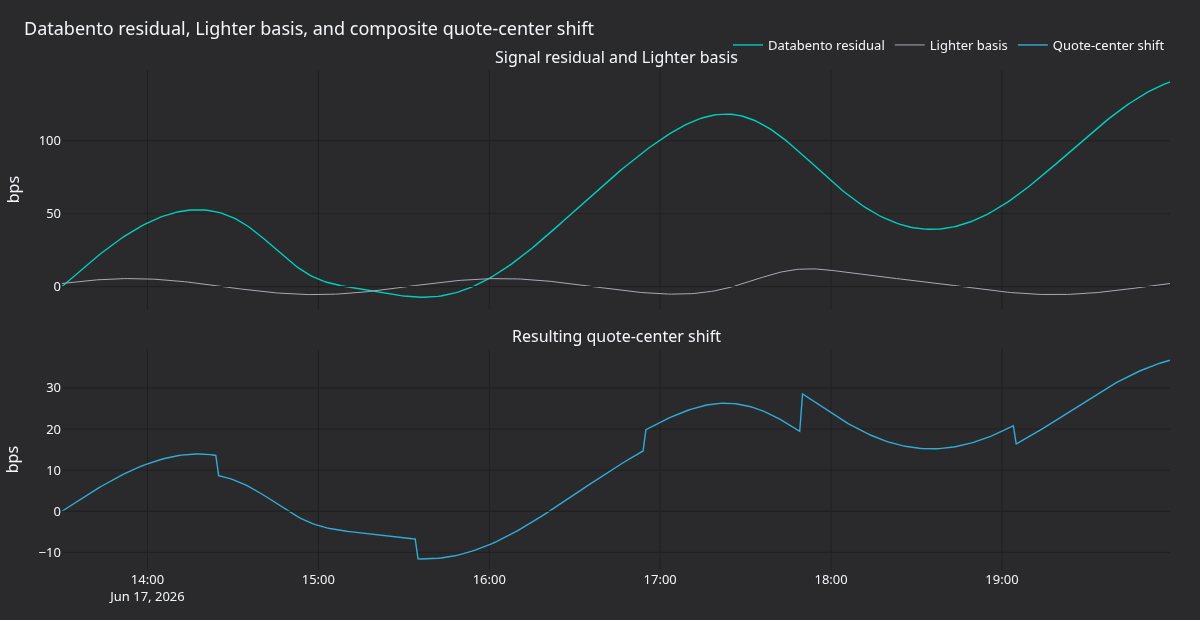

Figure 2. Databento residual, Lighter basis, and quote-center shift in bps.

Figure 3. Net position, signal shift, inventory adjustment, and total shift

for a 0.05 NVDA trade size and 0.20 NVDA position cap.

Figure 4. Lighter's continuous RWA market clock against the Databento US Equities cash-session signal, with signal age after the regular session.

Regenerate the panels

uv sync --extra visualization

python3 docs/tutorials/assets/lighter_rwa_composite_mm/render_panels.pyThe renderer writes four PNGs into

docs/tutorials/assets/lighter_rwa_composite_mm/. It uses the

nautilus_dark Plotly theme and deterministic replay data so docs builds do not

depend on vendor data licenses or live exchange access.

Extensions

The next useful improvement is a signal-age gate. For example, cancel all

Lighter orders when the latest NVDA.EQUS quote is older than 30 seconds during

the cash session, or immediately after the cash session closes. That makes the

Databento signal an explicit operating dependency instead of an implicit one.

For a pure fair-value strategy, use this tutorial as the client wiring and write a small variant that anchors bid/ask directly on the Databento mid, then checks the Lighter BBO only for post-only and basis limits.

Book Imbalance Backtest (Betfair)

This tutorial backtests a BookImbalanceActor on a Betfair MATCH_ODDS market. It loads a raw historical streaming .gz file, feeds it through the Rust...

Hurst/VPIN Directional Strategy (Kraken Futures)

This tutorial backtests a directional strategy on PF_XBTUSD, the USD-margined Bitcoin perpetual on Kraken Futures. The strategy combines a Hurst-exponent...