Book Imbalance Backtest (Betfair)

This is a Rust-only v2 system tutorial. It drives the Rust BacktestEngine

directly with raw Betfair streaming data, bypassing the Python and Parquet paths.

This tutorial backtests a BookImbalanceActor on a Betfair MATCH_ODDS market.

It loads a raw historical streaming .gz file, feeds it through the Rust

BacktestEngine, and tracks the bid/ask quoted-volume imbalance per runner.

Introduction

Betfair is a sports betting exchange where participants back (bid) and lay (ask) outcomes at decimal odds. Each runner has its own L2 order book that behaves like a financial order book.

The actor reads OrderBookDeltas for every runner and accumulates two

running totals per side: bid volume (back orders) and ask volume (lay

orders). Per-batch and cumulative imbalance are computed as:

imbalance = (bid_volume - ask_volume) / (bid_volume + ask_volume)A positive value means the market is leaning toward backing the outcome. Sports traders use this as a starting block, often combined with price momentum or market-wide features.

A release build processes about three million data points per second with full order book maintenance in the matching engine.

Prerequisites

- A working Rust toolchain (rustup.rs).

- The NautilusTrader repository cloned and building.

- A Betfair historical

.gzfile containing MCM (Market Change Message) data. Source it from Betfair historic data, a third-party archive, or by recording the Exchange Streaming API yourself.

Place the file at:

tests/test_data/local/betfair/1.253378068.gzThis path is gitignored and not shipped with the repository. The bundled example dataset is a football MATCH_ODDS market with 3 runners and around 82,000 MCM lines recorded over 18 days.

Loading the data

BetfairDataLoader reads gzip-compressed Betfair Exchange Streaming API

files and parses each line into Nautilus domain objects:

use nautilus_betfair::loader::{BetfairDataItem, BetfairDataLoader};

use nautilus_model::types::Currency;

let mut loader = BetfairDataLoader::new(Currency::GBP(), None);

let items = loader.load(&filepath)?;The loader returns a Vec<BetfairDataItem>:

| Variant | Description | Maps to Data enum? |

|---|---|---|

Instrument | Runner definition from market definition. | No (added separately) |

Status | Market status transition (PreOpen, Trading...). | No (Data has no variant) |

Deltas | Order book snapshot or delta update. | Yes, Data::Deltas |

Trade | Incremental trade tick from cumulative volumes. | Yes, Data::Trade |

Ticker | Last traded price, volume, BSP near/far. | - |

StartingPrice | Betfair Starting Price for a runner. | - |

BspBookDelta | BSP-specific book delta. | - |

InstrumentClose | Settlement event. | Yes, Data::InstrumentClose |

SequenceCompleted | Batch completion marker. | - |

RaceRunnerData | GPS tracking data (horse/greyhound racing). | - |

RaceProgress | Race‑level progress data. | - |

The backtest engine accepts the Data enum, so we map the variants we need

and skip the Betfair-specific types:

use nautilus_model::data::{Data, OrderBookDeltas_API};

let mut instruments = AHashMap::new();

let mut data: Vec<Data> = Vec::new();

for item in items {

match item {

BetfairDataItem::Instrument(inst) => {

instruments.insert(inst.id(), *inst);

}

BetfairDataItem::Deltas(d) => {

data.push(Data::Deltas(OrderBookDeltas_API::new(d)));

}

BetfairDataItem::Trade(t) => {

data.push(Data::Trade(t));

}

BetfairDataItem::InstrumentClose(c) => {

data.push(Data::InstrumentClose(c));

}

_ => {}

}

}OrderBookDeltas_API is a thin FFI wrapper around OrderBookDeltas

required by the Data enum.

Instruments are re-emitted on every market definition update in the stream, so the map deduplicates them by keeping the latest version.

The Status variant carries market status transitions (PreOpen, Trading,

Suspended, Closed) but the Data enum has no variant for it. This example

does not replay status transitions. If you extend this into a strategy that

places orders, the matching engine will not see market suspensions or

closures from the stream. Subscribe to instrument status separately or add

status routing to the engine.

The actor

NautilusTrader ships BookImbalanceActor in the trading crate's examples

module. The example wires it up with a per-runner instrument list and a

log interval:

use nautilus_trading::examples::actors::BookImbalanceActor;

let actor = BookImbalanceActor::new(instrument_ids, 5000, None);

engine.add_actor(actor)?;The second argument is the log interval: print a progress line every 5,000

updates per runner. The example reads IMBALANCE_LOG_INTERVAL from the

environment, so set it to a smaller value (200) when you want to capture

finer-grained data for the panels at the end of this tutorial.

The full source is at

crates/trading/src/examples/actors/imbalance/actor.rs.

How it works

A DataActor in Rust needs three pieces:

- A struct holding a

DataActorCorefield plus your own state. nautilus_actor!(YourType)to wire up the core, plus aDebugimplementation.- The

DataActortrait implementation with your callbacks.

The framework provides blanket Actor and Component implementations for

runtime actors. The nautilus_actor! macro supplies the native runtime wiring

when your struct holds a DataActorCore, so normal actor code only implements

the callbacks it needs.

On start the actor subscribes to OrderBookDeltas for each instrument. On

each update it sums per-side volume from the individual deltas and

accumulates running totals. On stop it prints a per-instrument summary.

Setting managed: false in subscribe_book_deltas means the data engine

does not maintain a separate order book copy in the cache for the actor.

The exchange-side matching engine still maintains its own book through

book.apply_delta() on every delta. Set managed: true if your actor

needs to read the full book state from

self.cache().order_book(&instrument_id).

Backtest engine setup

Create the engine and venue

Betfair is a cash-settled betting exchange. The venue uses

AccountType::Cash, OmsType::Netting, and BookType::L2_MBP:

let mut engine = BacktestEngine::new(BacktestEngineConfig::default())?;

engine.add_venue(

SimulatedVenueConfig::builder()

.venue(Venue::from("BETFAIR"))

.oms_type(OmsType::Netting)

.account_type(AccountType::Cash)

.book_type(BookType::L2_MBP)

.starting_balances(vec![Money::from("1_000_000 GBP")])

.build()?,

)?;Add instruments, actor, and data

for instrument in instruments.values() {

engine.add_instrument(instrument)?;

}

let actor = BookImbalanceActor::new(instrument_ids, 5000, None);

engine.add_actor(actor)?;

engine.add_data(data, None, true, true)?;The add_data parameters are (data, client_id, validate, sort). With

validate: true the engine checks the first element's instrument is

registered (the batch is assumed homogeneous). With sort: true it sorts

by timestamp.

Run

engine.run(None, None, None, false)?;The four parameters are (start, end, run_config_id, streaming). Passing

None for start/end uses the full time range of the loaded data.

What happens during the run

For each data point in timestamp order the engine:

- Advances the clock to the data timestamp.

- Routes the data to the simulated exchange, which applies each delta to

the per-instrument

OrderBookand runs the matching engine cycle. - Publishes the data through the data engine and message bus, triggering

the actor's

on_book_deltascallback. - Drains command queues and settles venues (processes any pending orders).

The matching engine maintains a full order book per instrument. The example

has no orders to match, so the book state is ready to use as soon as it is

swapped for a Strategy.

Results

The bundled MATCH_ODDS dataset has three runners and 143,098 data points; a release build completes in about 48 ms:

--- Book imbalance summary ---

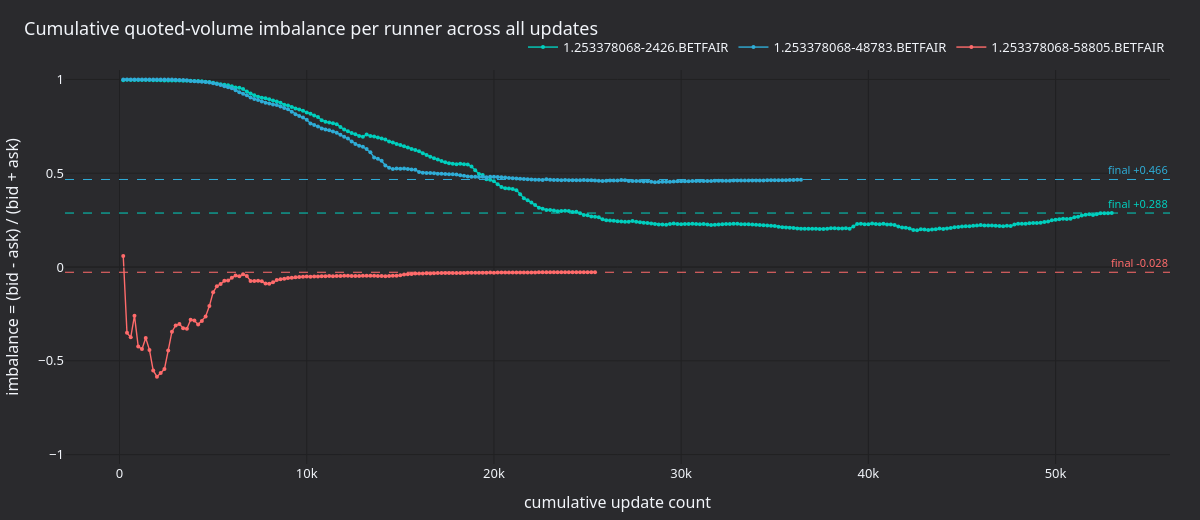

1.253378068-2426.BETFAIR updates: 53197 bid_vol: 212225339.34 ask_vol: 117422531.85 imbalance: 0.2876

1.253378068-48783.BETFAIR updates: 36475 bid_vol: 52506905.49 ask_vol: 19104694.72 imbalance: 0.4664

1.253378068-58805.BETFAIR updates: 25426 bid_vol: 24295351.82 ask_vol: 25692733.11 imbalance: -0.0280Runner 2426 (the eventual winner, settled at BSP 2.22) ends at +0.288:

backing flow dominates lay flow throughout the market. Runner 48783 shows

even stronger backing pressure (+0.466) over fewer updates, while 58805

ends close to neutral (-0.028).

Figure 1. Cumulative (bid - ask) / (bid + ask) per runner across the

~143k updates of the market lifetime. Dashed lines mark each runner's final

imbalance.

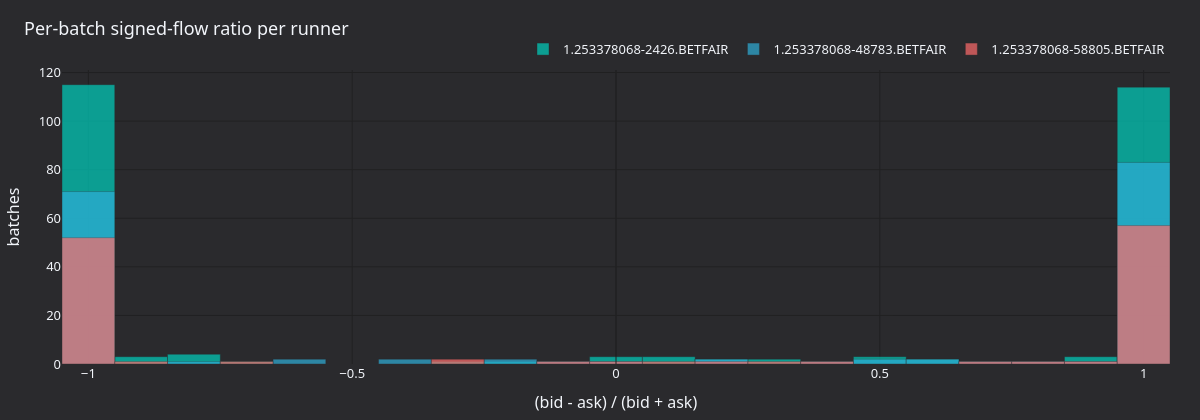

Figure 2. Distribution of per-batch signed flow ratio

(bid - ask) / (bid + ask) over IMBALANCE_LOG_INTERVAL=200 batches per

runner. The shape of each runner's batch distribution is a sharper signal

than the cumulative imbalance.

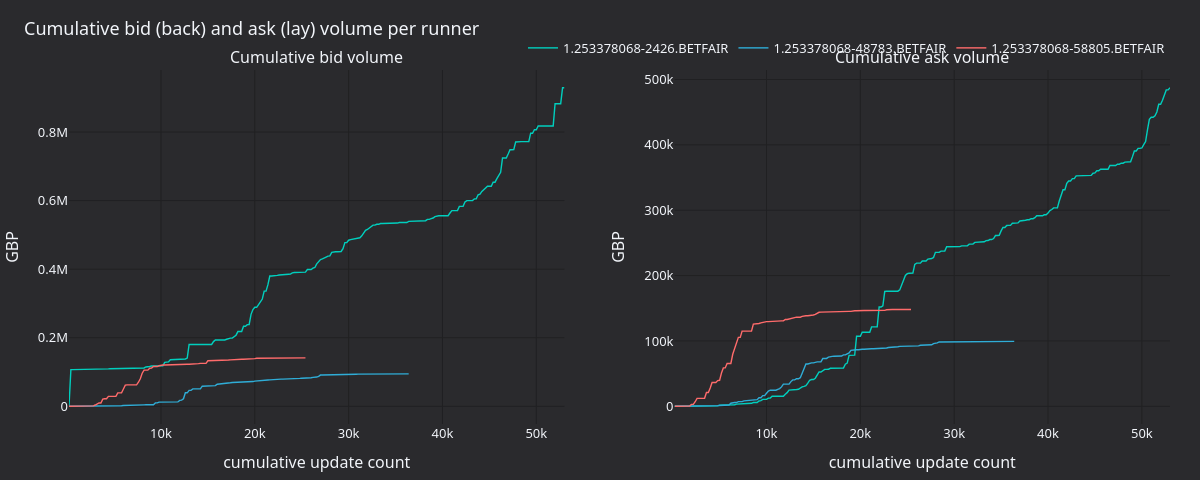

Figure 3. Cumulative back (bid) and lay (ask) volume per runner. Both sides are non-monotonic: lay flow occasionally outpaces back flow within short bursts even when cumulative imbalance stays positive.

Regenerate the panels

The actor logs [runner] update #N: batch bid=B ask=A cumulative imbalance=I

on every Nth update. The renderer parses those lines and writes static PNGs

using the nautilus_dark tearsheet theme.

IMBALANCE_LOG_INTERVAL=200 cargo run -p nautilus-betfair --features examples --release \

--example betfair-backtest > /tmp/betfair.log 2>&1

uv sync --extra visualization

BETFAIR_LOG=/tmp/betfair.log \

python3 docs/tutorials/assets/backtest_book_imbalance_betfair/render_panels.pyRunning the example

# Debug build

cargo run -p nautilus-betfair --features examples --example betfair-backtest

# Release build (recommended)

cargo run -p nautilus-betfair --features examples --release --example betfair-backtest

# Custom data file

cargo run -p nautilus-betfair --features examples --release --example betfair-backtest -- path/to/file.gzComplete source

The complete example is at

crates/adapters/betfair/examples/betfair_backtest.rs.

Next steps

- Add a strategy. Replace the actor with a

Strategyimplementation that places back/lay orders based on the imbalance signal. See theEmaCrossexample incrates/trading/src/examples/strategies/ema_cross/strategy.rsfor the pattern. - Use managed books. Set

managed: trueinsubscribe_book_deltasand read the full book viaself.cache().order_book(&id)for richer signals like top-of-book spread, depth ratios, or weighted mid-price. - Multiple markets. Load several

.gzfiles and run them through the same engine to test cross-market signals. - Compare with Python. Run the same backtest from Python using the

BacktestEnginePython API. The Rust engine processes the same data pipeline at roughly six times the throughput of the Python/Cython path.

Delta-Neutral Options Strategy (Derive)

This tutorial runs the shared DeltaNeutralVol strategy with the Derive adapter. The shipped example discovers ETH options, selects an out-of-the-money call...

Composite Market Making on Lighter RWA with Databento US Equities NVDA

This tutorial runs the shipped [CompositeMarketMaker][composite-market-maker] strategy on Lighter's NVDA-PERP.LIGHTER RWA market using Databento NVDA.EQUS...