Grid Market Making with a Deadman's Switch (BitMEX)

This tutorial backtests the shipped GridMarketMaker strategy on BitMEX

XBTUSD with free historical quote data from

Tardis.dev, then runs the same configuration live

through a Rust LiveNode. It focuses on BitMEX's deadman's switch: a

server-side cancel-all timer that protects the strategy from stranded

quotes if the client loses connectivity.

Introduction

XBTUSD is BitMEX's USD-denominated, BTC-margined inverse perpetual swap with a deep order book back to 2014. Tight spreads and predictable depth make it a natural venue for grid market making.

Why BitMEX for grid market making

Two adapter features land cleanly on this strategy:

- Deadman's switch (

cancelAllAfter): BitMEX maintains a server-side cancel-all timer. The execution client refreshes it on a schedule. If the link drops and the timer expires, BitMEX cancels every open order on the account. - Submit/cancel broadcaster: the adapter can fan out submissions and cancellations across multiple HTTP connections in parallel, with the first successful response short-circuiting the rest.

Deadman's switch mechanics

When deadmans_switch_timeout_secs is set, a background task continuously

refreshes the server-side timer at one-quarter of the timeout:

timeout = 60s -> refresh interval = timeout / 4 = 15s

t=0s Strategy starts, cancelAllAfter(60000ms) sent

t=15s Refresh: cancelAllAfter(60000ms) sent (resets timer)

t=30s Refresh: cancelAllAfter(60000ms) sent

t=45s Refresh: cancelAllAfter(60000ms) sent

t=50s Connectivity lost (last refresh was at t=45s)

t=105s Server timer fires -> BitMEX cancels all open ordersStranded quotes are a serious risk for market making: a crashed client

holding grid orders around mid can take an unbounded loss before manual

intervention. The deadman's switch caps the exposure window at timeout

seconds.

Prerequisites

- NautilusTrader installed.

- A Rust toolchain (

cargo) for the live example. Install from rustup.rs. - A BitMEX account: sign up at bitmex.com and generate an API key with order management permissions. Use the BitMEX testnet for first runs.

Environment variables

# Mainnet

export BITMEX_API_KEY="your-api-key"

export BITMEX_API_SECRET="your-api-secret"

# Testnet

export BITMEX_TESTNET_API_KEY="your-testnet-api-key"

export BITMEX_TESTNET_API_SECRET="your-testnet-api-secret"Alternatively place these in a .env file at the project root; both the

Python and Rust paths load it via dotenvy.

Backtesting with free Tardis quote data

BitMEX does not expose historical L2 data via its own API beyond recent trades. Tardis.dev captures and archives tick-level BitMEX data from March 2019 onward. The first day of each month is free to download without an API key.

Download the data

curl -L -o XBTUSD.csv.gz \

https://datasets.tardis.dev/v1/bitmex/quotes/2024/01/01/XBTUSD.csv.gz

curl -L -o XBTUSD-trades.csv.gz \

https://datasets.tardis.dev/v1/bitmex/trades/2024/01/01/XBTUSD.csv.gzThe trades file is optional for the strategy but useful for the panels: the matching engine needs aggressor flow to lift maker orders, which the trades stream supplies.

Full historical data (all dates) requires a paid Tardis API key. Use the Tardis download utility for bulk fetches.

Load the data

TardisCSVDataLoader parses the .csv.gz files directly:

from nautilus_trader.adapters.tardis.loaders import TardisCSVDataLoader

from nautilus_trader.model.identifiers import InstrumentId

instrument_id = InstrumentId.from_str("XBTUSD.BITMEX")

loader = TardisCSVDataLoader(instrument_id=instrument_id)

quotes = loader.load_quotes("XBTUSD.csv.gz")

trades = loader.load_trades("XBTUSD-trades.csv.gz")The instrument_id argument tags every record as XBTUSD.BITMEX

regardless of how it is keyed in the source CSV.

Instrument definition

XBTUSD is an inverse perpetual: prices are quoted in USD, but the contract is margined and settled in BTC. One contract represents 1 USD of notional exposure.

from decimal import Decimal

from nautilus_trader.model.currencies import BTC

from nautilus_trader.model.currencies import USD

from nautilus_trader.model.enums import AssetClass

from nautilus_trader.model.identifiers import Symbol

from nautilus_trader.model.instruments import PerpetualContract

from nautilus_trader.model.objects import Price

from nautilus_trader.model.objects import Quantity

XBTUSD = PerpetualContract(

instrument_id=instrument_id,

raw_symbol=Symbol("XBTUSD"),

underlying="XBT",

asset_class=AssetClass.CRYPTOCURRENCY,

base_currency=BTC,

quote_currency=USD,

settlement_currency=BTC,

is_inverse=True,

price_precision=1,

size_precision=0,

price_increment=Price.from_str("0.5"),

size_increment=Quantity.from_int(1),

multiplier=Quantity.from_int(1),

lot_size=Quantity.from_int(1),

margin_init=Decimal("0.01"),

margin_maint=Decimal("0.005"),

maker_fee=Decimal("-0.00025"),

taker_fee=Decimal("0.00075"),

ts_event=0,

ts_init=0,

)Fee rates are explicit backtest assumptions. Check bitmex.com/app/fees for current rates.

Backtest engine setup

XBTUSD is BTC-margined, so the starting balance is in BTC:

from nautilus_trader.backtest.config import BacktestEngineConfig

from nautilus_trader.backtest.engine import BacktestEngine

from nautilus_trader.config import LoggingConfig

from nautilus_trader.model.enums import AccountType

from nautilus_trader.model.enums import OmsType

from nautilus_trader.model.identifiers import TraderId

from nautilus_trader.model.identifiers import Venue

from nautilus_trader.model.objects import Money

engine = BacktestEngine(

BacktestEngineConfig(

trader_id=TraderId("BACKTESTER-001"),

logging=LoggingConfig(log_level="INFO"),

),

)

BITMEX = Venue("BITMEX")

engine.add_venue(

venue=BITMEX,

oms_type=OmsType.NETTING,

account_type=AccountType.MARGIN,

base_currency=BTC,

starting_balances=[Money(1, BTC)],

)

engine.add_instrument(XBTUSD)

engine.add_data(quotes + trades)Strategy configuration

from nautilus_trader.examples.strategies.grid_market_maker import GridMarketMaker

from nautilus_trader.examples.strategies.grid_market_maker import GridMarketMakerConfig

strategy = GridMarketMaker(

GridMarketMakerConfig(

instrument_id=instrument_id,

max_position=Quantity.from_int(300),

trade_size=Quantity.from_int(100),

num_levels=3,

grid_step_bps=100,

skew_factor=0.5,

requote_threshold_bps=10,

),

)

engine.add_strategy(strategy)Run and review results

import pandas as pd

engine.run()

with pd.option_context("display.max_rows", 100, "display.max_columns", None, "display.width", 300):

print(engine.trader.generate_account_report(BITMEX))

print(engine.trader.generate_order_fills_report())

print(engine.trader.generate_positions_report())

engine.reset()

engine.dispose()The complete backtest script is at

bitmex_grid_market_maker.py.

What the run produces

The free 2024-01-01 sample is a quiet New Year's Day session: BTC traded

in a roughly 200-USD range across most of the day. With the

recommended-for-live grid_step_bps=100 (1%) the inner buy and sell levels

sit ~420 USD from mid and never get touched: the example completes with

zero fills, which is the honest outcome on a calm session.

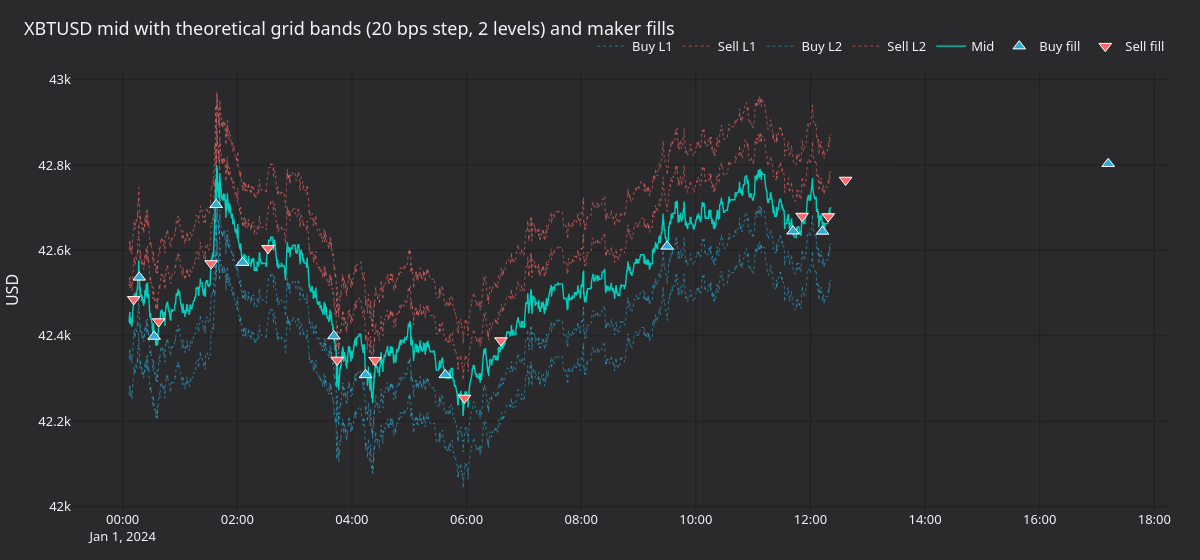

The panels below use a tighter grid_step_bps=20 configuration on the

first 200,000 quotes so the maker fills are visible. With 20 bps step,

two levels, and 20 bps requote threshold, the strategy fires 22 maker

fills across the captured window.

Figure 1. XBTUSD mid (teal) with the four theoretical grid bands at

grid_step_bps=20, num_levels=2. Triangles are maker fills, up = buy,

down = sell.

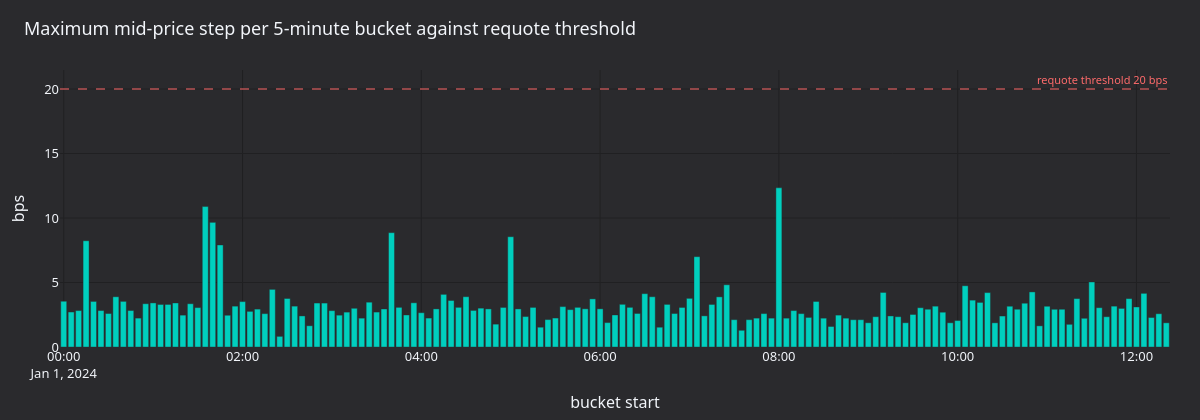

Figure 2. Maximum mid step (in basis points) per 5-minute bucket across the captured window. Buckets above the dashed line crossed the requote threshold at least once.

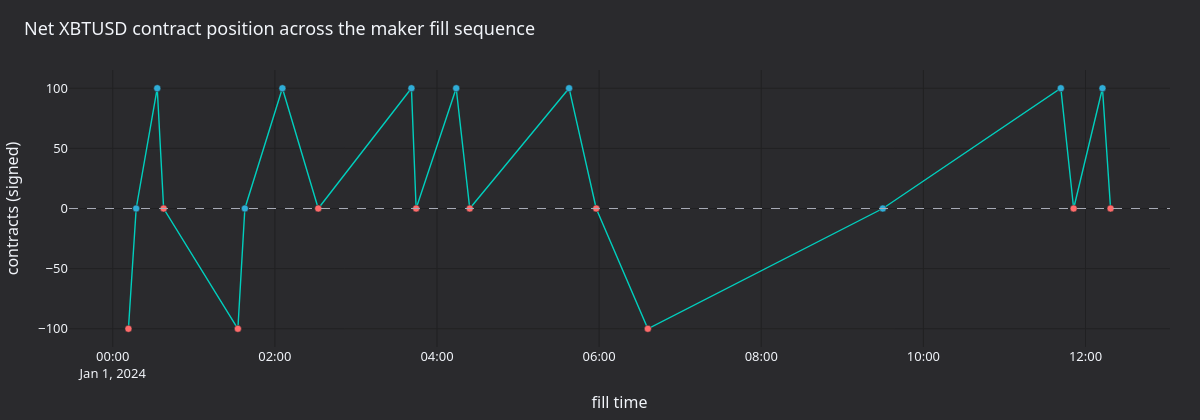

Figure 3. Cumulative signed XBTUSD contracts across the maker fill sequence. Inventory skew pulls the grid back toward flat after each fill.

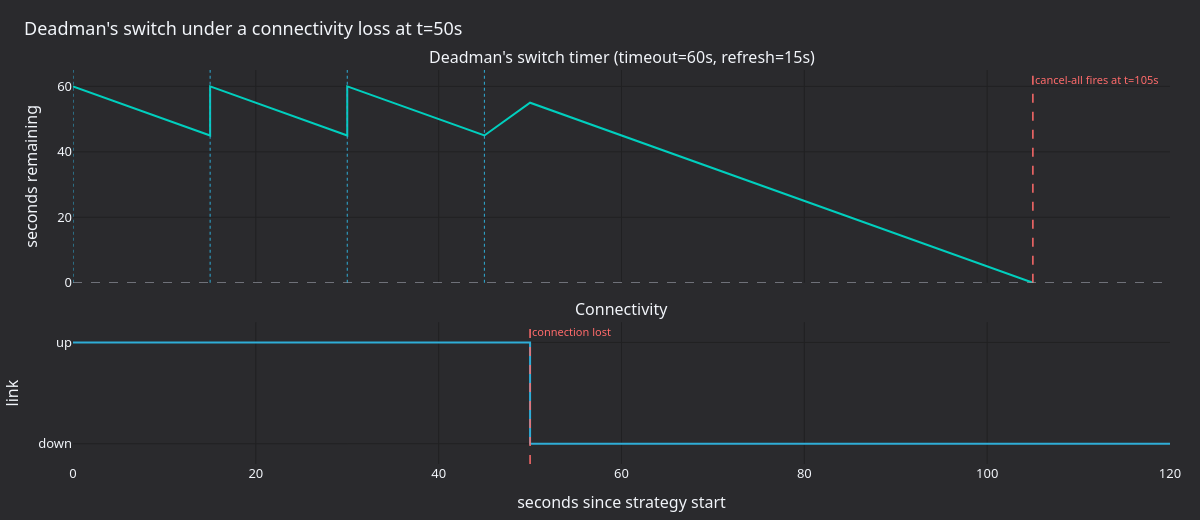

Figure 4. Server-side cancel-all timer with timeout=60s,

refresh_interval=15s. Refreshes reset the timer to 60s. After connectivity

fails at t=50s the timer drains uninterrupted; the server fires

cancelAll at t=105s.

Regenerate the panels

uv sync --extra visualization

XBTUSD_QUOTES=XBTUSD.csv.gz XBTUSD_TRADES=XBTUSD-trades.csv.gz \

python3 docs/tutorials/assets/grid_market_maker_bitmex/render_panels.pyThe renderer caps the dataset at 200,000 quotes and 30,000 trades to keep the run reproducible in a few minutes.

Live trading: GridMarketMaker with deadman's switch

After the backtest behaves, the same configuration runs live through the

Rust LiveNode. The strategy is implemented natively in Rust.

Environment setup

Credentials load automatically from environment variables when not set explicitly in the config:

# Testnet (recommended for first runs)

export BITMEX_TESTNET_API_KEY="your-key"

export BITMEX_TESTNET_API_SECRET="your-secret"Or place them in a .env file at the project root.

Code walkthrough

The complete main() function is at

node_grid_mm.rs:

#[tokio::main]

async fn main() -> Result<(), Box<dyn std::error::Error>> {

dotenvy::dotenv().ok();

let environment = Environment::Live;

let trader_id = TraderId::from("TESTER-001");

let instrument_id = InstrumentId::from("XBTUSD.BITMEX");

let data_config = BitmexDataClientConfig {

environment: BitmexEnvironment::Testnet,

..Default::default()

};

let exec_config = BitmexExecFactoryConfig::new(

trader_id,

BitmexExecClientConfig {

environment: BitmexEnvironment::Testnet,

deadmans_switch_timeout_secs: Some(60),

..Default::default()

},

);

let data_factory = BitmexDataClientFactory::new();

let exec_factory = BitmexExecutionClientFactory::new();

let log_config = LoggerConfig {

stdout_level: LevelFilter::Info,

..Default::default()

};

let mut node = LiveNode::builder(trader_id, environment)?

.with_logging(log_config)

.add_data_client(None, Box::new(data_factory), Box::new(data_config))?

.add_exec_client(None, Box::new(exec_factory), Box::new(exec_config))?

.with_reconciliation(true)

.with_reconciliation_lookback_mins(2880)

.with_delay_post_stop_secs(5)

.build()?;

let config = GridMarketMakerConfig::builder()

.instrument_id(instrument_id)

.max_position(Quantity::from("300"))

.num_levels(3)

.grid_step_bps(100)

.skew_factor(0.5)

.requote_threshold_bps(10)

.build();

let strategy = GridMarketMaker::new(config);

node.add_strategy(strategy)?;

node.run().await?;

Ok(())

}Configuration points:

deadmans_switch_timeout_secs: Some(60): arms the deadman's switch with a 60-second timeout and a 15-second refresh interval.with_reconciliation(true): queries the BitMEX REST API on startup to reload open orders and positions, so the strategy resumes correctly after a restart.with_reconciliation_lookback_mins(2880): reconciliation looks back 2880 minutes (two days) of order history.with_delay_post_stop_secs(5): 5-second grace period after stop for pending cancel and fill events to settle before the node exits.

BitMEX-specific considerations

GTC orders and post-only

BitMEX grid orders are submitted as GTC with

ParticipateDoNotInitiate (post-only). If the price has crossed the book

by the time the order arrives, BitMEX rejects it rather than letting it

take liquidity.

This differs from the dYdX setup, where short-term orders provide

automatic expiry every 8 seconds. On BitMEX the requote cycle is driven

entirely by mid-price movement (requote_threshold_bps).

Order quantization

Price and size quantization for BitMEX instruments is handled automatically by the adapter. No manual rounding or conversion is needed in strategy code.

Inverse perpetual accounting

XBTUSD is BTC-margined. PnL accrues in BTC: a one-USD spread captured at

a 42,000 USD price earns 1/42,000 BTC per fill. Size max_position and

trade_size accordingly.

Run the example

cargo run --example bitmex-grid-mm --package nautilus-bitmex --features examplesGraceful shutdown

Press Ctrl+C to stop the node. The shutdown sequence:

- SIGINT received, trader stops,

on_stop()fires. - Strategy cancels all orders and closes positions.

- 5-second grace period (

delay_post_stop_secs) processes residual events. - Deadman's switch background task stops.

- Clients disconnect, node exits.

Configuration reference

GridMarketMaker parameters

| Parameter | Type | Default | Description |

|---|---|---|---|

instrument_id | InstrumentId | required | Instrument to trade (e.g. XBTUSD.BITMEX). |

max_position | Quantity | required | Maximum net exposure in contracts (long or short). |

trade_size | Quantity | None | Size per grid level. If None, uses instrument's min_quantity or 1.0. |

num_levels | usize | 3 | Number of buy and sell levels. |

grid_step_bps | u32 | 10 | Grid spacing in basis points (100 = 1%). |

skew_factor | f64 | 0.0 | How aggressively to shift the grid based on net inventory. |

requote_threshold_bps | u32 | 5 | Minimum mid‑price move (bps) before re‑quoting. |

expire_time_secs | Option<u64> | None | Order expiry in seconds. Use None for GTC on BitMEX. |

on_cancel_resubmit | bool | false | Resubmit grid on next quote after an unexpected cancel. |

Deadman's switch parameter

| Parameter | Type | Description |

|---|---|---|

deadmans_switch_timeout_secs | Option<u64> | Server‑side cancel timer in seconds. Refresh interval = timeout / 4 (minimum 1s). None disables the feature. |

A 60-second timeout gives a 15-second refresh interval and a 60-second window before BitMEX fires the timer. Lower values reduce the exposure window but increase API call frequency; higher values reduce overhead but extend the window.

Choosing grid parameters

grid_step_bps: XBTUSD has tight spreads. Start at 50-100 bps to ensure fills before tightening. Each level captures half the step as spread.skew_factor: start at0.0(no skew). A value of0.5shifts the grid by 0.5 USD per contract of net position.requote_threshold_bps: 10 bps (0.1%) is a starting point for XBTUSD. Lower values cause cancel/replace churn; higher values leave orders stale during fast moves.

Event flow

Monitoring and understanding output

Key log messages

| Log message | Meaning |

|---|---|

Requoting grid: mid=X, last_mid=Y | Mid moved beyond threshold, refreshing grid. |

Starting dead man's switch: timeout=60s, refresh_interval=15s | Deadman's switch armed at node start. |

Dead man's switch heartbeat failed: ... | Transient network issue; switch will retry next interval. |

Disarming dead man's switch | Switch stopped cleanly during shutdown. |

benign cancel error, treating as success | Cancel for an already‑filled or cancelled order (normal). |

Reconciling orders from last 2880 minutes | Startup reconciliation loading prior state. |

Expected behaviour patterns

- Startup: instruments load, reconciliation queries prior orders, WebSocket connects, first quote triggers initial grid.

- Steady state: grid persists across ticks; requotes only when mid moves beyond threshold.

- Fills: position updates, skew adjusts on next requote.

- Shutdown: all orders cancelled, positions closed, deadman's switch stops.

- Restart: reconciliation restores open order state; strategy resumes from prior grid.

Customization tips

High vs low volatility

| Condition | Adjustment |

|---|---|

| High volatility | Wider grid_step_bps (100-200), fewer num_levels, lower skew_factor. |

| Low volatility | Tighter grid_step_bps (20-50), more num_levels, higher skew_factor. |

| Thin liquidity | Increase requote_threshold_bps to reduce cancel frequency. |

Enabling the submit broadcaster

For production deployments, enable the submit broadcaster to provide redundant order submission across multiple HTTP connections:

let exec_config = BitmexExecFactoryConfig::new(

trader_id,

BitmexExecClientConfig {

environment: BitmexEnvironment::Mainnet,

deadmans_switch_timeout_secs: Some(60),

submitter_pool_size: Some(2),

canceller_pool_size: Some(2),

..Default::default()

},

);With submitter_pool_size=2, each order submission fans out to two HTTP

clients in parallel; the first successful response wins. This reduces the

probability of a missed submission when one path stalls.

Mainnet toggle

Switch networks by setting the environment field on both configs to

BitmexEnvironment::Mainnet. All endpoints and credential environment

variables resolve automatically.

Further reading

- BitMEX integration guide: full adapter reference.

- On-chain grid market making with short-term orders (dYdX): short-term order expiry as an alternative to the deadman's switch.

- Tardis downloadable CSV files: schema documentation for the Tardis archives.

- BitMEX API documentation:

cancelAllAfterendpoint and order management reference.

Gold Perpetual Book Imbalance with Proxy Futures Data (AX Exchange)

This tutorial backtests a top-of-book imbalance strategy on XAU-PERP at AX Exchange using Databento CME gold futures (GC.v.0) mbp-1 quotes as a proxy.

On-Chain Grid Market Making with Short-Term Orders (dYdX)

This tutorial runs the shipped GridMarketMaker strategy on dYdX v4 through the Rust LiveNode. The strategy places symmetric limit orders around the mid...