Delta-Neutral Options Strategy (Bybit)

This is a Rust-only v2 system tutorial. It runs a live delta-neutral

short-volatility strategy on Bybit using the Rust LiveNode.

This tutorial runs a short OTM strangle on Bybit BTC options and delta-hedges with the BTCUSDT perpetual. The strategy selects call and put strikes at startup, enters via implied-volatility limit orders, tracks portfolio delta from venue-provided Greeks, and submits market hedge orders on the perpetual when the delta drifts beyond a threshold.

This strategy trades real money on mainnet. Setting enter_strangle: false

only disables the initial strangle entry orders. The strategy still

hydrates existing positions from the cache at startup and still submits

hedge orders on the perpetual when portfolio delta breaches the

threshold. If the account holds option or hedge positions from a prior

session, the strategy will trade.

Prerequisites

- Completion of the options data tutorial, which

covers instrument discovery, Greeks subscriptions, and the

DataActorpattern. - A Bybit API key with trading permissions for options and linear perpetuals.

- Environment variables:

export BYBIT_API_KEY="your-api-key"

export BYBIT_API_SECRET="your-api-secret"Strategy overview

The DeltaNeutralVol strategy ships in the trading crate's examples

module and runs in five stages:

- Strike selection: queries the instrument cache for all BTC options, filters to the nearest expiry, selects OTM call and put strikes by percentile rank.

- Entry: places SELL limit orders on both legs priced by implied

volatility (via Bybit's

order_ivparameter). Entry is optional and disabled by default in the example. - Greeks tracking: subscribes to

OptionGreeksfor both legs. Deltas and IVs come directly from Bybit's option ticker stream. - Rehedging: computes portfolio delta and submits a market order on the BTCUSDT perpetual when the threshold is breached. Triggers on every Greeks update and on a periodic safety timer.

- Position tracking: tracks call, put, and hedge positions via

on_order_filled. Hydrates existing positions from the cache at startup.

Portfolio delta

The strategy computes net exposure as:

portfolio_delta = call_delta * call_position

+ put_delta * put_position

+ hedge_positionA short strangle starts near delta-neutral because the call and put

deltas offset. With the default target_call_delta = 0.20 and

target_put_delta = -0.20, the two legs cancel at entry. As the

underlying moves, net delta drifts and the strategy hedges to bring it

back toward zero.

Configuration

The example file at

crates/adapters/bybit/examples/node_delta_neutral.rs

configures the strategy:

let hedge_instrument_id = InstrumentId::from("BTCUSDT-LINEAR.BYBIT");

let strategy_config = DeltaNeutralVolConfig::builder()

.option_family("BTC".to_string())

.hedge_instrument_id(hedge_instrument_id)

.client_id(client_id)

.contracts(1)

.rehedge_delta_threshold(0.5)

.rehedge_interval_secs(30)

.enter_strangle(false)

.iv_param_key("order_iv".to_string())

.build();

let strategy = DeltaNeutralVol::new(strategy_config);Parameters (defaults shown are the struct defaults; the example

overrides enter_strangle to false and iv_param_key to

"order_iv"):

| Parameter | Default | Example | Description |

|---|---|---|---|

option_family | required | "BTC" | Underlying filter for instrument discovery. |

hedge_instrument_id | required | BTCUSDT-LINEAR | Perpetual used for delta hedging. |

client_id | required | "BYBIT" | Data and execution client identifier. |

target_call_delta | 0.20 | - | Target call delta for strike selection. |

target_put_delta | -0.20 | - | Target put delta for strike selection. |

contracts | 1 | - | Contracts per leg. |

rehedge_delta_threshold | 0.5 | - | Portfolio delta that triggers a hedge. |

rehedge_interval_secs | 30 | - | Periodic rehedge timer interval. |

enter_strangle | true | false | Place entry orders when Greeks arrive. |

entry_iv_offset | 0.0 | - | Vol points below mark IV for entry pricing. |

iv_param_key | "px_vol" | "order_iv" | Adapter‑specific IV parameter key. |

The iv_param_key is the key difference between venues. Bybit uses

order_iv, which the adapter maps to the orderIv field in the

place-order API. OKX uses px_vol. Setting this correctly is required

for IV-based order placement.

Node setup

The example configures both data and execution clients with Option and

Linear product types:

let data_config = BybitDataClientConfig {

api_key: None,

api_secret: None,

product_types: vec![BybitProductType::Option, BybitProductType::Linear],

..Default::default()

};

let exec_config = BybitExecClientConfig {

api_key: None,

api_secret: None,

product_types: vec![BybitProductType::Option, BybitProductType::Linear],

account_id: Some(account_id),

..Default::default()

};Both product types are needed: Option for the strangle legs, Linear

for the BTCUSDT perpetual hedge instrument. The execution client requires

account_id for order identity tracking.

let mut node = LiveNode::builder(trader_id, environment)?

.with_name("BYBIT-DELTA-NEUTRAL-001".to_string())

.add_data_client(None, Box::new(data_factory), Box::new(data_config))?

.add_exec_client(None, Box::new(exec_factory), Box::new(exec_config))?

.with_reconciliation(true)

.with_delay_post_stop_secs(5)

.build()?;

node.add_strategy(strategy)?;

node.run().await?;with_reconciliation(true) queries Bybit at startup for open orders and

positions, hydrating the cache before the strategy starts. The strategy

then picks up any existing positions from a prior session.

How the strategy works

Strike selection

On start the strategy queries the cache for all option instruments

matching option_family. It discards expired options, selects the

nearest expiry, separates calls and puts, and sorts each list by strike

price.

Strikes are chosen by percentile in the sorted list:

- Call: index =

(1.0 - target_call_delta) * count. With 0.20 target delta and 50 calls, this selects the 40th strike (80th percentile, OTM). - Put: index =

|target_put_delta| * count. With -0.20 target delta, this selects the 10th strike (20th percentile, OTM).

This is a heuristic. Strike price ordering approximates delta ordering for options at the same expiry. A production strategy would subscribe to Greeks for all strikes first, then select by actual delta.

Entry via implied volatility

When enter_strangle is true and both mark IVs have arrived, the

strategy places SELL limit orders using the order_iv parameter:

let mut call_params = Params::new();

call_params.insert("order_iv".to_string(), json!(call_entry_iv.to_string()));

self.submit_order(call_order, None, Some(client_id), Some(call_params))?;Bybit converts orderIv to a limit price server-side and gives it

priority over any explicit price. The entry_iv_offset config subtracts

vol points from mark IV: an offset of 0.02 sells two vol points below

mark for faster fills.

Bybit's demo environment rejects orders with order_iv. The adapter

denies them before they reach the API. Use mainnet or testnet for

IV-based order placement.

Rehedging

Two triggers check portfolio delta:

- Every Greeks update:

on_option_greeksrecomputes portfolio delta after updating the leg's delta value. - Periodic timer: fires every

rehedge_interval_secsas a safety net when Greeks updates stop arriving.

When |portfolio_delta| > rehedge_delta_threshold, the strategy submits

a market order on the hedge instrument. A hedge_pending flag prevents

duplicate submissions while an order is in flight.

Position tracking

The strategy tracks positions via on_order_filled, not by querying

the cache on every tick. Each fill updates the corresponding position

counter (call, put, or hedge). At startup, existing positions are

hydrated from the cache (populated by reconciliation).

Shutdown

On stop the strategy cancels open orders, unsubscribes from all data feeds, and resets the hedge-pending flag. It does not close positions. Unwinding the strangle and hedge requires manual action or a separate exit strategy.

What the run produces

A 30-second mainnet run with enter_strangle: false against a clean

account places no orders. The strategy logs the discovered instruments

and the strike selection:

Selected call: BTC-28APR26-81000-C-USDT-OPTION.BYBIT (strike=81000)

Selected put: BTC-28APR26-75000-P-USDT-OPTION.BYBIT (strike=75000)

Strangle: 1 contracts per leg, hedge on BTCUSDT-LINEAR.BYBITThat is enough to reason about the strategy's structural behaviour. The panels below visualise the mechanics around the actual selected strikes (75,000 / 81,000) at the captured underlying.

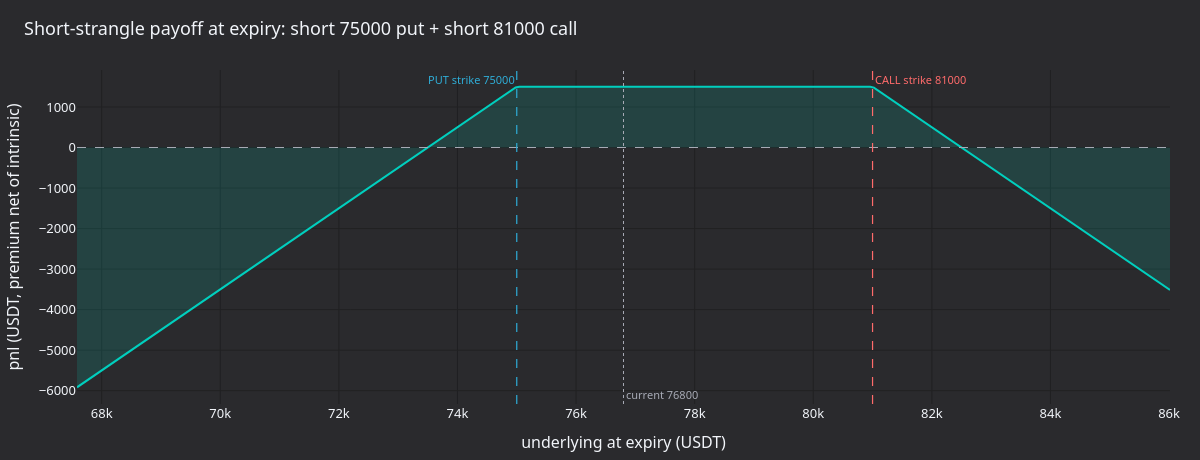

Figure 1. Pnl at expiry of the short 75,000 PUT plus short 81,000 CALL combination, assuming a 1,500 USDT total premium and zero discount. The flat top is the credit-only zone between strikes; loss grows linearly past either strike.

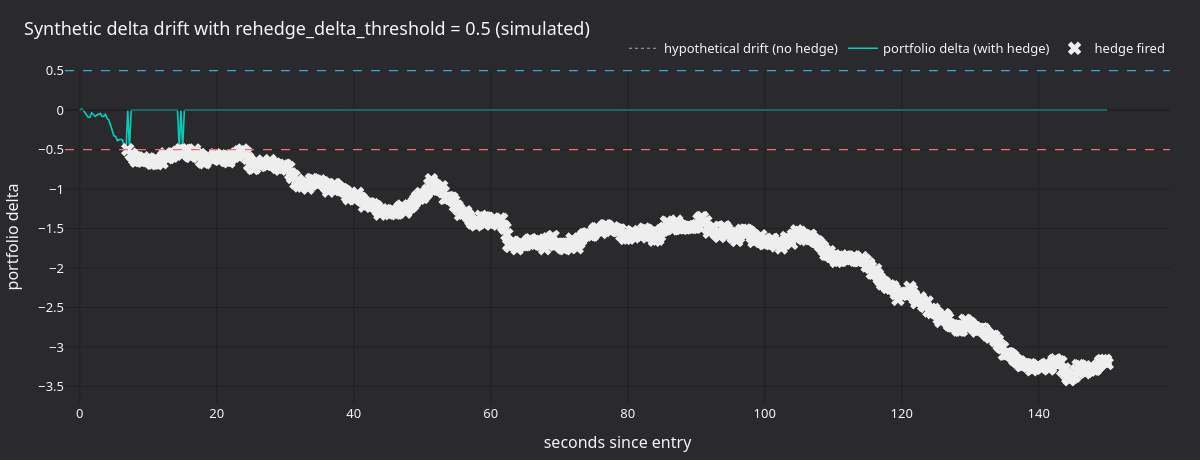

Figure 2. Synthetic Brownian delta drift over 150 seconds with

rehedge_delta_threshold=0.5. The dotted curve is the un-hedged drift;

the line is the strategy's portfolio delta after each market hedge fire

(crosses).

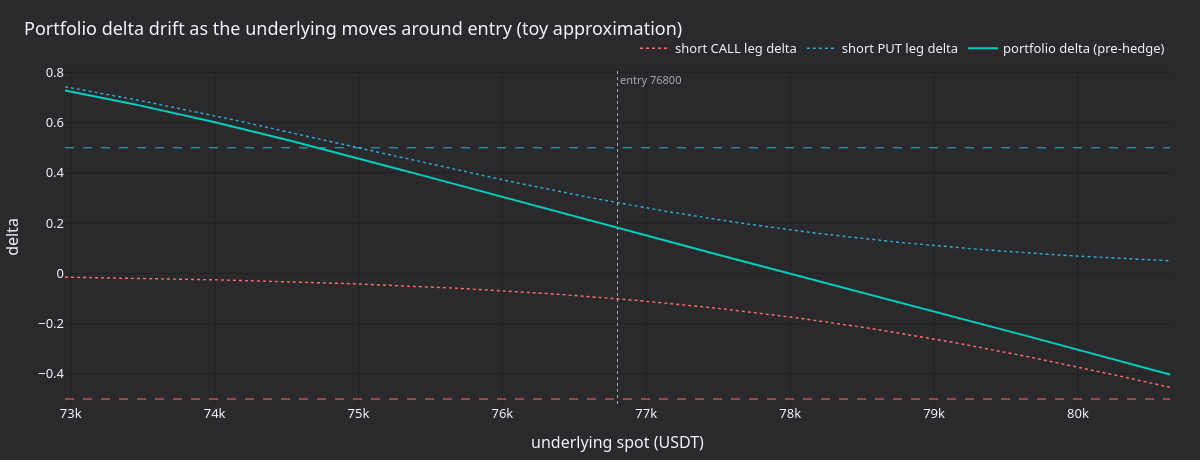

Figure 3. Toy approximation of how the short call and short put leg deltas move with a 5% spot range around entry, plus the resulting portfolio delta before hedging. Negative gamma compresses the curve in the wings and steepens it across the strikes.

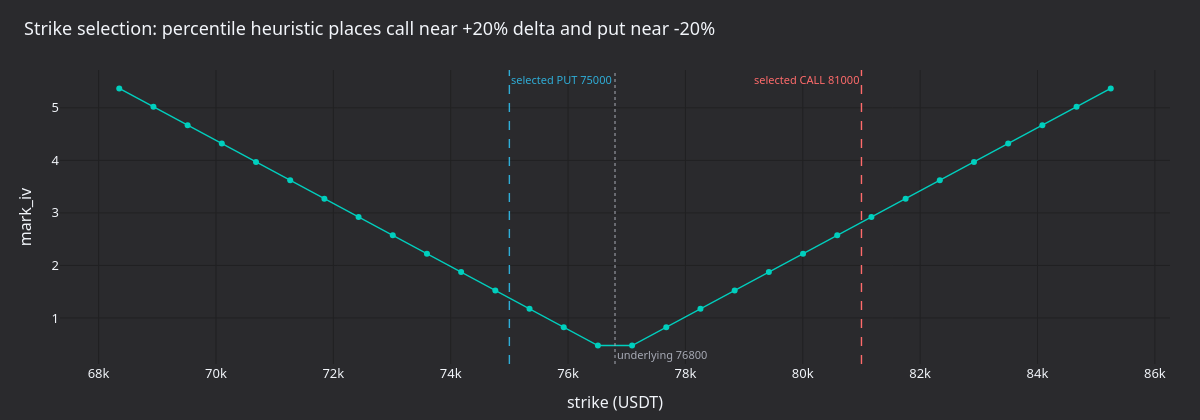

Figure 4. The strike-selection heuristic against an illustrative IV smile. The CALL strike sits at the (1 - 0.20) percentile and the PUT at the 0.20 percentile, placing both legs OTM at roughly equal-magnitude deltas around the underlying.

Regenerate the panels

timeout 30 ./target/release/examples/bybit-delta-neutral > /tmp/bybit_dn.log 2>&1

uv sync --extra visualization

DN_LOG=/tmp/bybit_dn.log \

python3 docs/tutorials/assets/delta_neutral_options_bybit/render_panels.pyThe renderer parses selected strikes from the log; the panels themselves are illustrative because the default config does not place orders.

Risk considerations

- Gamma risk: a short strangle has negative gamma. Large underlying

moves increase delta exposure faster than the rehedge timer responds.

Tighten

rehedge_delta_thresholdand reducerehedge_interval_secsfor faster response, at the cost of more hedge trades. - Vega risk: an IV spike increases mark-to-market loss on the short options. The strategy does not manage vega exposure.

- Liquidity: OTM crypto options can have wide spreads. Hedge quality degrades when the underlying gaps or the perpetual trades in coarse size increments.

- Lifecycle risk: stopping the strategy stops hedging. Positions remain open and unhedged until manually managed.

Running the example

cargo run --example bybit-delta-neutral --package nautilus-bybit --features examplesThe example runs with enter_strangle: false by default, so it does not

place strangle entry orders. It still hydrates existing positions and

submits hedge orders if portfolio delta breaches the threshold. On a

clean account with no prior positions, no orders are placed.

Stop with Ctrl+C. The strategy cancels open orders and unsubscribes before shutdown.

Complete source

- Example runner:

crates/adapters/bybit/examples/node_delta_neutral.rs - Strategy implementation:

crates/trading/src/examples/strategies/delta_neutral_vol/ - Strategy README with full config reference:

crates/trading/src/examples/strategies/delta_neutral_vol/README.md

See also

- Options data and Greeks on Bybit: prerequisite tutorial covering Greeks subscriptions and option chain snapshots.

- Options: option instrument types and data architecture.

- Bybit integration: options

order parameters including

order_ivandmmp.

Options Data and Greeks (Bybit)

This tutorial connects to Bybit's live options market and consumes Greeks and option chain data through two DataActor examples. It covers instrument...

Delta-Neutral Options Strategy (Derive)

This tutorial runs the shared DeltaNeutralVol strategy with the Derive adapter. The shipped example discovers ETH options, selects an out-of-the-money call...