Mean Reversion with Proxy FX Data (AX Exchange)

This tutorial backtests a Bollinger-band mean-reversion strategy on EURUSD-PERP at AX Exchange using TrueFX EUR/USD spot ticks as a proxy.

Introduction

The strategy combines two indicators on 1-minute mid bars:

- Bollinger Bands (

BBMeanReversion'sBB(20, 2.0sd)): a rolling 20-bar mean and a +/-2sd envelope. The bands flag price as overextended relative to recent volatility. - Relative Strength Index (

RSI(14)): a 14-bar momentum oscillator. NautilusTrader RSI is on[0, 1], so the conventional 30/70 thresholds become0.30/0.70.

Entry needs both signals at once: a touch of the lower band with RSI < 0.30

opens a long; a touch of the upper band with RSI > 0.70 opens a short.

Exit is one-sided: any open position closes when the close crosses back

through the BB middle. Existing positions on the opposite side are flattened

before a new entry.

The shipped BBMeanReversion strategy is intentionally simple and has no

edge.

Why proxy data

AX Exchange is a new venue not yet covered by historical data vendors. TrueFX publishes free, institutional-grade EUR/USD spot tick archives (Integral and Jefferies pools) that stand in cleanly for AX EURUSD-PERP backtests.

Prerequisites

- Python 3.12+

- NautilusTrader installed.

- A free TrueFX account, used to download a monthly tick archive.

Data preparation

Download TrueFX EUR/USD ticks

- Go to the TrueFX historical downloads page.

- Pick EUR/USD and a month, for example December 2025.

- Extract the ZIP. The CSV is headerless with columns

pair, timestamp, bid, ask.

Load into Nautilus quote ticks

from pathlib import Path

import pandas as pd

from nautilus_trader.persistence.wranglers import QuoteTickDataWrangler

df = pd.read_csv(

Path("EURUSD-2025-12.csv"),

header=None,

names=["pair", "timestamp", "bid", "ask"],

)

df["timestamp"] = pd.to_datetime(df["timestamp"], format="%Y%m%d %H:%M:%S.%f")

df = df.set_index("timestamp")[["bid", "ask"]]

wrangler = QuoteTickDataWrangler(instrument=EURUSD_PERP) # defined below

ticks = wrangler.process(df)The wrangler tags every tick with the instrument ID. The strategy declares

1-MINUTE-MID-INTERNAL, so the engine builds 1-minute MID bars from the

tick stream internally.

Instrument definition

Proxy data needs a manual instrument definition. The multiplier of 1000

gives one contract a notional of 1,000 EUR.

from decimal import Decimal

from nautilus_trader.model.currencies import USD

from nautilus_trader.model.enums import AssetClass

from nautilus_trader.model.identifiers import InstrumentId

from nautilus_trader.model.identifiers import Symbol

from nautilus_trader.model.instruments import PerpetualContract

from nautilus_trader.model.objects import Price

from nautilus_trader.model.objects import Quantity

instrument_id = InstrumentId.from_str("EURUSD-PERP.AX")

EURUSD_PERP = PerpetualContract(

instrument_id=instrument_id,

raw_symbol=Symbol("EURUSD-PERP"),

underlying="EUR",

asset_class=AssetClass.FX,

quote_currency=USD,

settlement_currency=USD,

is_inverse=False,

price_precision=5,

size_precision=0,

price_increment=Price.from_str("0.00001"),

size_increment=Quantity.from_int(1),

multiplier=Quantity.from_int(1000),

lot_size=Quantity.from_int(1),

margin_init=Decimal("0.05"),

margin_maint=Decimal("0.025"),

maker_fee=Decimal("0.0002"),

taker_fee=Decimal("0.0005"),

ts_event=0,

ts_init=0,

)Fees and margin are explicit backtest assumptions. Check the AX Exchange documentation for current rates.

Configuration

| Parameter | Value | Description |

|---|---|---|

bb_period | 20 | Rolling window for the BB mean and the standard deviation. |

bb_std | 2.0 | Band width in standard deviations. |

rsi_period | 14 | RSI lookback in bars. |

rsi_buy_threshold | 0.30 | Long entry confirmation (NautilusTrader RSI is [0, 1]). |

rsi_sell_threshold | 0.70 | Short entry confirmation. |

trade_size | 1 | One contract per trade (1,000 EUR notional). |

NautilusTrader RSI returns values in [0.0, 1.0], not [0, 100]. The

0.30 / 0.70 thresholds correspond to the textbook 30 / 70 levels.

Backtest setup

from nautilus_trader.backtest.config import BacktestEngineConfig

from nautilus_trader.backtest.engine import BacktestEngine

from nautilus_trader.config import LoggingConfig

from nautilus_trader.examples.strategies.bb_mean_reversion import BBMeanReversion

from nautilus_trader.examples.strategies.bb_mean_reversion import BBMeanReversionConfig

from nautilus_trader.model.data import BarType

from nautilus_trader.model.enums import AccountType

from nautilus_trader.model.enums import OmsType

from nautilus_trader.model.identifiers import TraderId

from nautilus_trader.model.identifiers import Venue

from nautilus_trader.model.objects import Money

engine = BacktestEngine(

BacktestEngineConfig(

trader_id=TraderId("BACKTESTER-001"),

logging=LoggingConfig(log_level="INFO"),

),

)

AX = Venue("AX")

engine.add_venue(

venue=AX,

oms_type=OmsType.NETTING,

account_type=AccountType.MARGIN,

base_currency=USD,

starting_balances=[Money(100_000, USD)],

)

engine.add_instrument(EURUSD_PERP)

engine.add_data(ticks)

strategy = BBMeanReversion(

BBMeanReversionConfig(

instrument_id=instrument_id,

bar_type=BarType.from_str("EURUSD-PERP.AX-1-MINUTE-MID-INTERNAL"),

trade_size=Decimal("1"),

bb_period=20,

bb_std=2.0,

rsi_period=14,

rsi_buy_threshold=0.30,

rsi_sell_threshold=0.70,

),

)

engine.add_strategy(strategy)

engine.run()Reports come straight off engine.trader:

print(engine.trader.generate_account_report(AX))

print(engine.trader.generate_order_fills_report())

print(engine.trader.generate_positions_report())

engine.reset()

engine.dispose()The runnable example is at

architect_ax_mean_reversion.py.

What the run produces

Replaying TrueFX EUR/USD December 2025 through BBMeanReversion(20, 2sd, RSI 14)

prints 44,591 1-minute mid bars and closes 1,089 positions across 2,178 fills.

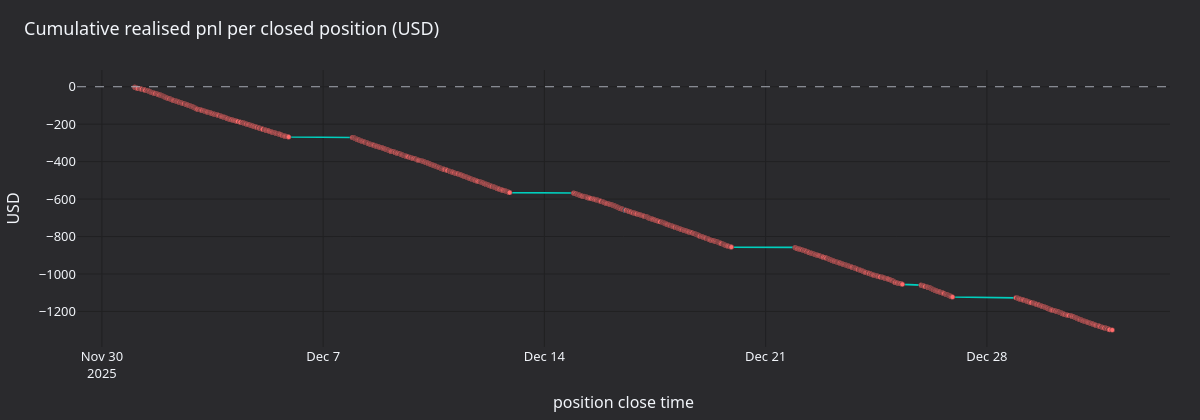

Cumulative realised pnl ends at -1,287 USD: the strategy bleeds steadily

through the month with no clear regime-driven recovery. Mean reversion

without a regime filter pays the spread on every cycle, and EUR/USD ran a

pronounced uptrend through the second half of December which the strategy

fought repeatedly.

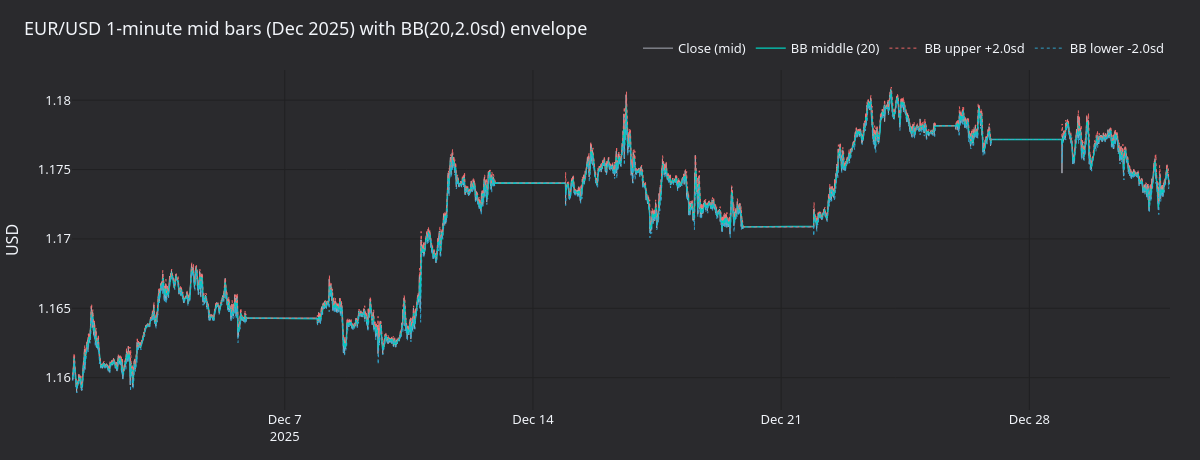

Figure 1. EUR/USD 1-minute mid bars across December 2025 with the BB middle and +/-2sd envelope. Long flat patches are weekend gaps in the TrueFX feed.

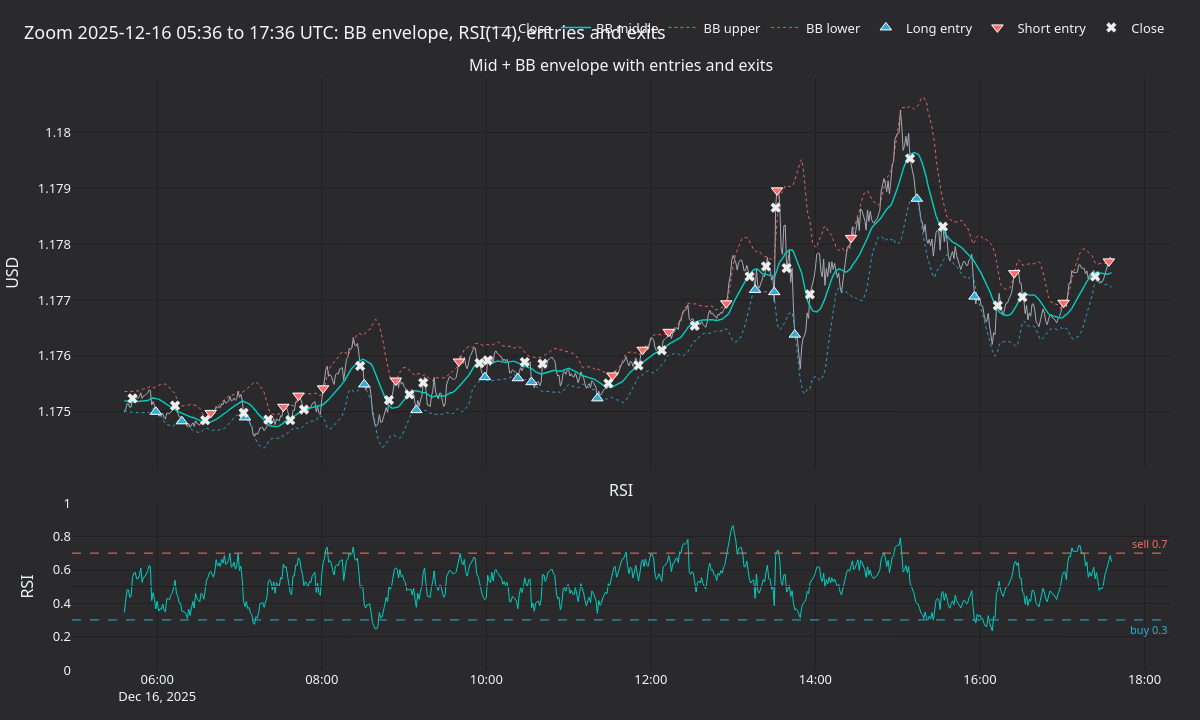

Figure 2. Twelve-hour zoom around the dataset midpoint. Top: mid with BB envelope, long entries (triangles up), short entries (triangles down), and closing fills (crosses). Bottom: RSI(14) with the 0.30 buy / 0.70 sell thresholds.

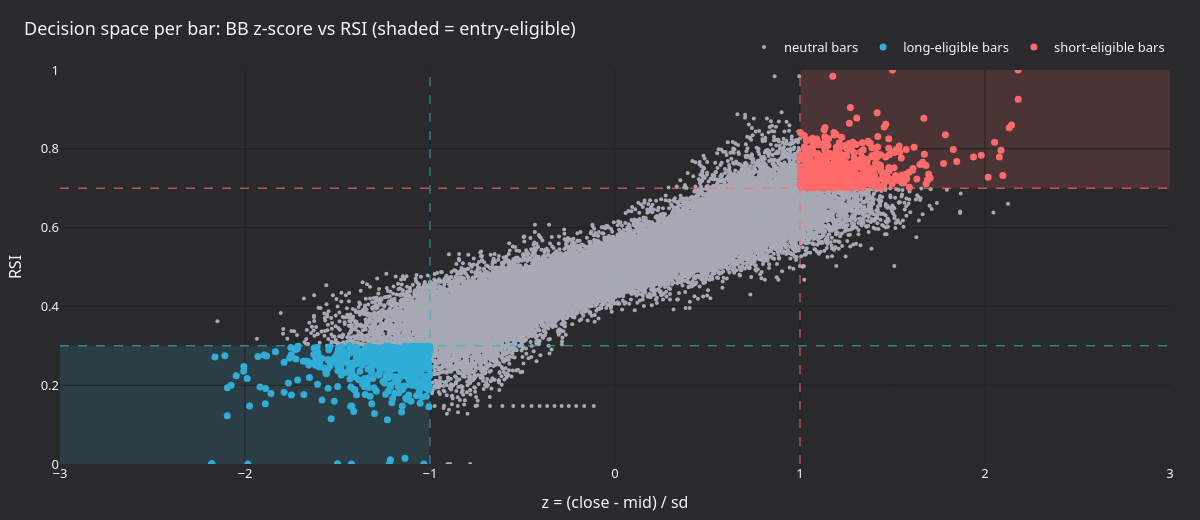

Figure 3. Per-bar BB z-score against RSI for the whole month. Shaded regions mark the entry-eligible quadrants: lower-left (long) and upper-right (short). The diagonal lobe is the natural co-movement of band-relative price and RSI.

Figure 4. Cumulative realised USD pnl across closed positions. The curve declines roughly linearly, dominated by spread and small adverse moves on each cycle.

Regenerate the panels

A self-contained renderer re-runs the backtest, computes BB and RSI on the

captured bars, and writes PNG panels using the shared nautilus_dark

tearsheet theme.

uv sync --extra visualization

TRUEFX_CSV=tests/test_data/local/truefx/EURUSD-2025-12.csv \

python3 docs/tutorials/assets/fx_mean_reversion_ax/render_panels.pySet TRUEFX_CSV to wherever you saved the EUR/USD archive.

Next steps

- Add a regime filter. The drawdown is concentrated in trending sessions. Suppress entries when realised range or a slower trend filter says the market is directional.

- Tune thresholds. A wider band (

bb_std=2.5) or stricter RSI cutoffs (0.25/0.75) cut entries but raise the bar for confirmation. - Add stops. Hard stop-loss orders cap downside per cycle and prevent carrying a losing position to the BB middle reversion.

- Go live on the AX sandbox. Connect to the AX sandbox for paper trading once the backtest behaves. See the AX Exchange integration guide for setup.

Running live

The same BBMeanReversion strategy runs live against AX Exchange. The

launch script swaps the BacktestEngine for a TradingNode with the AX

data and execution clients configured. See the live example:

ax_mean_reversion.py.

For connection setup and API key configuration, see the AX Exchange integration guide.