Options Data and Greeks (Bybit)

This is a Rust-only v2 system tutorial. It uses the Rust LiveNode

with the Bybit adapter to stream live option Greeks and aggregated chain

snapshots.

This tutorial connects to Bybit's live options market and consumes Greeks

and option chain data through two DataActor examples. It covers

instrument discovery, venue-provided Greeks subscriptions, and periodic

chain snapshots with ATM-relative strike filtering.

Introduction

Bybit publishes Greeks (delta, gamma, vega, theta) and implied volatility alongside every option ticker update. NautilusTrader exposes this data at two levels:

- Per-instrument Greeks: subscribe to a single option contract and

receive an

OptionGreeksevent on every ticker update. - Option chain snapshots: subscribe to an entire expiry series and

receive periodic

OptionChainSliceevents that aggregate quotes and Greeks across all active strikes.

Two example binaries back these patterns: the first subscribes to individual Greeks streams, the second subscribes to an aggregated chain with ATM-relative strike filtering.

Prerequisites

- A working Rust toolchain (rustup.rs).

- The NautilusTrader repository cloned and building.

- A Bybit API key with read permissions. No trading permissions are needed for data-only use. Create keys at bybit.com.

- Environment variables set for authentication:

export BYBIT_API_KEY="your-api-key"

export BYBIT_API_SECRET="your-api-secret"A .env file in the repository root also works. The examples load it via

dotenvy.

Bybit demo trading uses stream-demo.bybit.com only for private streams.

Public option market data uses the mainnet public stream

wss://stream.bybit.com/v5/public/option.

The DataActor pattern

A Rust DataActor needs three pieces:

- A struct with a

core: DataActorCorefield plus your own state. - The

nautilus_actor!(YourType)macro plus aDebugimplementation. - A

DataActortrait implementation with your callbacks.

The macro supplies the native runtime wiring required by the blanket Actor

and Component implementations, so you only implement the callbacks you need.

Every callback has a default no-op implementation.

Part 1: per-instrument Greeks

The bybit-greeks-tester example subscribes to OptionGreeks for all

BTC CALL options at the nearest expiry and logs each update.

Actor structure

#[derive(Debug)]

struct GreeksTester {

core: DataActorCore,

client_id: ClientId,

subscribed_instruments: Vec<InstrumentId>,

}

nautilus_actor!(GreeksTester);

impl GreeksTester {

fn new(client_id: ClientId) -> Self {

Self {

core: DataActorCore::new(DataActorConfig {

actor_id: Some("GREEKS_TESTER-001".into()),

..Default::default()

}),

client_id,

subscribed_instruments: Vec::new(),

}

}

}The core field is required by the macro. The client_id identifies

which data client to route subscriptions to. The subscribed_instruments

vector tracks what we subscribed to so we clean up on stop.

Discovering instruments

On start, the actor queries the cache for all option instruments, filters for BTC CALLs that have not expired, and finds the nearest expiry:

fn on_start(&mut self) -> anyhow::Result<()> {

let venue = Venue::new("BYBIT");

let underlying_filter = Ustr::from("BTC");

let mut options: Vec<(InstrumentId, f64, u64)> = {

let cache = self.cache();

let instruments = cache.instruments(&venue, Some(&underlying_filter));

instruments

.iter()

.filter_map(|inst| {

if inst.option_kind() == Some(OptionKind::Call) {

let expiry = inst.expiration_ns()?.as_u64();

let strike = inst.strike_price()?.as_f64();

Some((inst.id(), strike, expiry))

} else {

None

}

})

.collect()

}; // cache borrow dropped here

let now_ns = self.timestamp_ns().as_u64();

options.retain(|(_, _, exp)| *exp > now_ns);

let nearest_expiry = options.iter().map(|(_, _, exp)| *exp).min().unwrap();

options.retain(|(_, _, exp)| *exp == nearest_expiry);

options.sort_by(|(_, a, _), (_, b, _)| a.partial_cmp(b).unwrap());

// ...subscribe to each

}Release the cache borrow before calling any subscription methods. The

cache uses Rc<RefCell<...>> internally, and subscription methods may

need to borrow it. Collect owned data into a local Vec, drop the cache

reference, then subscribe.

Subscribing to Greeks

After discovering instruments, subscribe to each one:

let client_id = self.client_id;

for (instrument_id, _, _) in &options {

self.subscribe_option_greeks(*instrument_id, Some(client_id), None);

self.subscribed_instruments.push(*instrument_id);

}Handling updates

Each ticker update from Bybit triggers on_option_greeks with an

OptionGreeks event:

fn on_option_greeks(&mut self, greeks: &OptionGreeks) -> anyhow::Result<()> {

log::info!(

"GREEKS | {} | delta={:.4} gamma={:.6} vega={:.4} theta={:.4} rho={:.6} | \

mark_iv={} bid_iv={} ask_iv={} | underlying={} oi={}",

greeks.instrument_id,

greeks.delta,

greeks.gamma,

greeks.vega,

greeks.theta,

greeks.rho,

greeks.mark_iv.map_or("-".to_string(), |v| format!("{v:.2}")),

greeks.bid_iv.map_or("-".to_string(), |v| format!("{v:.2}")),

greeks.ask_iv.map_or("-".to_string(), |v| format!("{v:.2}")),

greeks.underlying_price.map_or("-".to_string(), |v| format!("{v:.2}")),

greeks.open_interest.map_or("-".to_string(), |v| format!("{v:.1}")),

);

Ok(())

}The OptionGreeks fields:

| Field | Type | Description |

|---|---|---|

instrument_id | InstrumentId | The option contract. |

delta | f64 | Price sensitivity to underlying. |

gamma | f64 | Delta sensitivity to underlying. |

vega | f64 | Price sensitivity to a 1% change in volatility. |

theta | f64 | Daily time decay. |

rho | f64 | Sensitivity to interest rate changes. |

mark_iv | Option<f64> | Mark price implied volatility. |

bid_iv | Option<f64> | Bid implied volatility. |

ask_iv | Option<f64> | Ask implied volatility. |

underlying_price | Option<f64> | Current underlying forward price for this expiry. |

open_interest | Option<f64> | Open interest for this contract. |

The delta, gamma, vega, theta, and rho values live on a nested

greeks: OptionGreekValues struct. OptionGreeks implements

Deref<Target = OptionGreekValues>, so greeks.delta and friends work

as shown above.

Bybit does not provide rho; the adapter sets it to 0.0.

Cleanup

On stop, unsubscribe from all instruments:

fn on_stop(&mut self) -> anyhow::Result<()> {

let ids: Vec<InstrumentId> = self.subscribed_instruments.drain(..).collect();

let client_id = self.client_id;

for instrument_id in ids {

self.unsubscribe_option_greeks(instrument_id, Some(client_id), None);

}

log::info!("Unsubscribed from all option greeks");

Ok(())

}Part 2: option chain snapshots

The bybit-option-chain example subscribes to an aggregated option chain

and logs periodic snapshots showing calls and puts at each strike with

their quotes and Greeks.

Why use option chains

Per-instrument subscriptions give granular control, but monitoring an

entire surface means managing individual streams and correlating updates

across strikes. An option chain subscription handles this: the

DataEngine aggregates quotes and Greeks across all strikes in a series

and publishes a single OptionChainSlice on a timer.

This aggregation happens inside NautilusTrader. Bybit publishes per-contract option market data and does not expose a native option chain stream in the V5 public WebSocket docs.

Key types

OptionSeriesId identifies a single expiry series:

let series_id = OptionSeriesId::new(

Venue::new("BYBIT"), // venue

Ustr::from("BTC"), // underlying

Ustr::from("USDT"), // settlement currency

UnixNanos::from(expiry), // expiration timestamp

);StrikeRange controls which strikes are active:

| Variant | Description |

|---|---|

Fixed | A fixed set of strike prices. |

AtmRelative | strikes_above above and strikes_below below ATM. |

AtmPercent | All strikes within pct of the ATM price. |

For ATM-based variants, subscriptions are deferred until the ATM price is determined from the venue-provided forward price.

Subscribing

let strike_range = StrikeRange::AtmRelative {

strikes_above: 3,

strikes_below: 3,

};

let snapshot_interval_ms = Some(5_000); // snapshot every 5 seconds

self.subscribe_option_chain(

series_id,

strike_range,

snapshot_interval_ms,

Some(client_id),

None, // params

);Pass None for snapshot_interval_ms to use raw mode, where every

quote or Greeks update publishes a slice immediately.

Handling snapshots

The on_option_chain callback receives an OptionChainSlice containing

all active strikes with their call and put data:

fn on_option_chain(&mut self, slice: &OptionChainSlice) -> anyhow::Result<()> {

log::info!(

"OPTION_CHAIN | {} | atm={} | calls={} puts={} | strikes={}",

slice.series_id,

slice.atm_strike.map_or("-".to_string(), |p| format!("{p}")),

slice.call_count(),

slice.put_count(),

slice.strike_count(),

);

for strike in slice.strikes() {

let call_info = slice.get_call(&strike).map(|d| {

let greeks_str = d.greeks.as_ref().map_or("-".to_string(), |g| {

format!(

"d={:.3} g={:.5} v={:.2} iv={:.1}%",

g.delta, g.gamma, g.vega,

g.mark_iv.unwrap_or(0.0) * 100.0,

)

});

format!("bid={} ask={} [{}]", d.quote.bid_price, d.quote.ask_price, greeks_str)

});

let put_info = slice.get_put(&strike).map(|d| {

let greeks_str = d.greeks.as_ref().map_or("-".to_string(), |g| {

format!(

"d={:.3} g={:.5} v={:.2} iv={:.1}%",

g.delta, g.gamma, g.vega,

g.mark_iv.unwrap_or(0.0) * 100.0,

)

});

format!("bid={} ask={} [{}]", d.quote.bid_price, d.quote.ask_price, greeks_str)

});

log::info!(

" K={} | CALL: {} | PUT: {}",

strike,

call_info.unwrap_or_else(|| "-".to_string()),

put_info.unwrap_or_else(|| "-".to_string()),

);

}

Ok(())

}The OptionChainSlice fields and methods:

| Name | Type / Returns | Description |

|---|---|---|

series_id | OptionSeriesId | The series this snapshot covers. |

atm_strike | Option<Price> | ATM strike from the forward price. |

call_count() | usize | Number of call strikes with data. |

put_count() | usize | Number of put strikes with data. |

strike_count() | usize | Union of all strikes. |

strikes() | Vec<Price> | Sorted list of all strike prices. |

get_call(k) | Option<&OptionStrikeData> | Call quote and Greeks at strike k. |

get_put(k) | Option<&OptionStrikeData> | Put quote and Greeks at strike k. |

Each OptionStrikeData contains a quote: QuoteTick (bid/ask) and an

optional greeks: Option<OptionGreeks>.

Node setup

Both examples use the same LiveNode pattern. No execution client is

needed for data-only use:

#[tokio::main]

async fn main() -> Result<(), Box<dyn std::error::Error>> {

dotenvy::dotenv().ok();

let environment = Environment::Live;

let trader_id = TraderId::test_default();

let client_id = ClientId::new("BYBIT");

let bybit_config = BybitDataClientConfig {

api_key: None, // loaded from BYBIT_API_KEY env var

api_secret: None, // loaded from BYBIT_API_SECRET env var

product_types: vec![BybitProductType::Option],

..Default::default()

};

let client_factory = BybitDataClientFactory::new();

let mut node = LiveNode::builder(trader_id, environment)?

.with_name("BYBIT-OPTIONS-001".to_string())

.add_data_client(None, Box::new(client_factory), Box::new(bybit_config))?

.with_delay_post_stop_secs(5)

.build()?;

let actor = GreeksTester::new(client_id); // or OptionChainTester

node.add_actor(actor)?;

node.run().await?;

Ok(())

}Setting product_types to [BybitProductType::Option] loads only option

instruments. Startup blocks while the instrument provider fetches and

parses every listed option.

Running the examples

# Per-instrument Greeks

cargo run --example bybit-greeks-tester --package nautilus-bybit --features examples

# Option chain snapshots

cargo run --example bybit-option-chain --package nautilus-bybit --features examplesStop either example with Ctrl+C. The actor's on_stop callback

unsubscribes from all streams before shutdown.

What the examples produce

A 30-second mainnet run on April 28 (BTC near 76,800 USDT, expiry 2026-04-28 08

UTC) captures 938 Greeks updates across 22 BTC CALL contracts in the per-instrument tester, plus 5 chain snapshots covering 7 strikes each in the chain tester.Per-instrument Greeks output

Found 22 BTC CALL options at nearest expiry (ts=1777359600000000000)

Subscribed to option greeks for 22 instruments

GREEKS | BTC-28APR26-72000-C-USDT-OPTION.BYBIT | delta=0.4733 gamma=0.000000 vega=0.0000 theta=-0.0000 rho=0.000000 | mark_iv=0.66 bid_iv=0.00 ask_iv=5.00 | underlying=76782.43 oi=0.0

GREEKS | BTC-28APR26-71000-C-USDT-OPTION.BYBIT | delta=0.4733 gamma=0.000000 vega=0.0000 theta=-0.0000 rho=0.000000 | mark_iv=0.74 bid_iv=0.00 ask_iv=5.00 | underlying=76782.43 oi=0.1

GREEKS | BTC-28APR26-73000-C-USDT-OPTION.BYBIT | delta=0.4733 gamma=0.000000 vega=0.0000 theta=-0.0000 rho=0.000000 | mark_iv=0.57 bid_iv=0.00 ask_iv=5.00 | underlying=76782.43 oi=0.0Option chain output

OPTION_CHAIN | BYBIT:BTC:USDT:2026-04-28T08:00:00Z | atm=77000 | calls=7 puts=7 | strikes=7

K=75500 | CALL: bid=1210 ask=1430 [d=0.445 g=0.00000 v=0.00 iv=36.2%] | PUT: bid=0 ask=5 [d=0.000 g=0.00000 v=0.00 iv=36.2%]

K=76000 | CALL: bid=700 ask=850 [d=0.445 g=0.00000 v=0.00 iv=32.5%] | PUT: bid=0 ask=5 [d=0.000 g=0.00000 v=0.00 iv=32.5%]

K=76500 | CALL: bid=265 ask=370 [d=0.442 g=0.00000 v=0.07 iv=29.9%] | PUT: bid=0 ask=5 [d=-0.003 g=0.00000 v=0.07 iv=29.9%]Panels

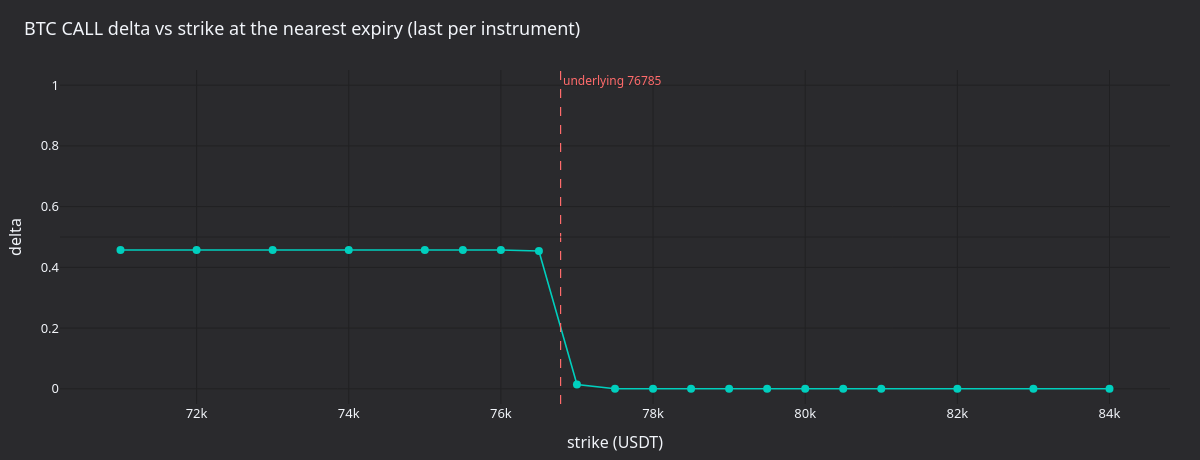

Figure 1. Last delta per BTC CALL strike at the nearest expiry, underlying ~77,000 USDT marked. Delta drops from ~0.45 below the underlying to near zero past the underlying. Bybit's delta on near-zero gamma contracts close to expiry compresses to a step-like profile around the forward.

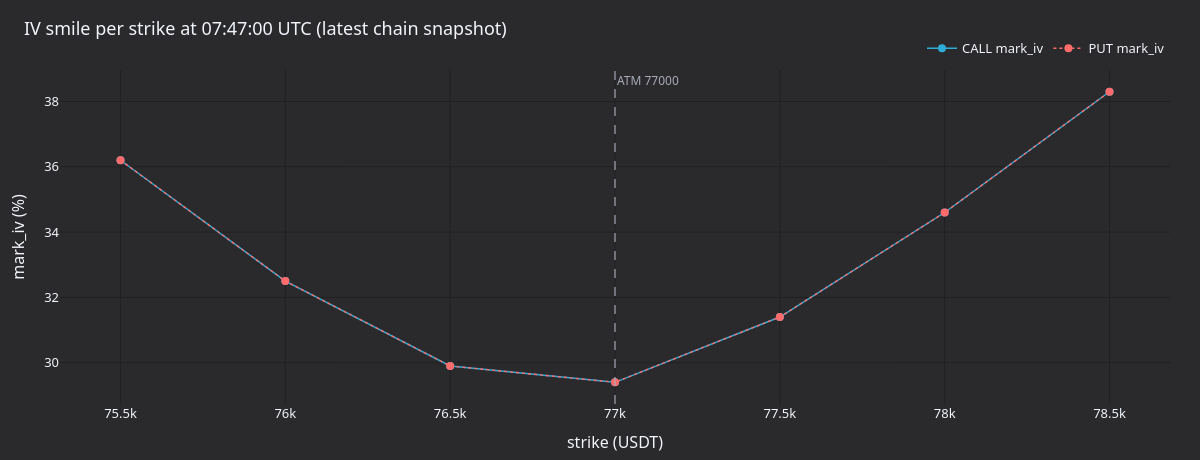

Figure 2. Mark IV per strike for the latest chain snapshot (CALL and PUT overlaid). The smile is symmetric around ATM at 77,000 USDT, with IV dipping from 36% at 75,500 to 30% at 77,000 and rising back to 38% at 78,500.

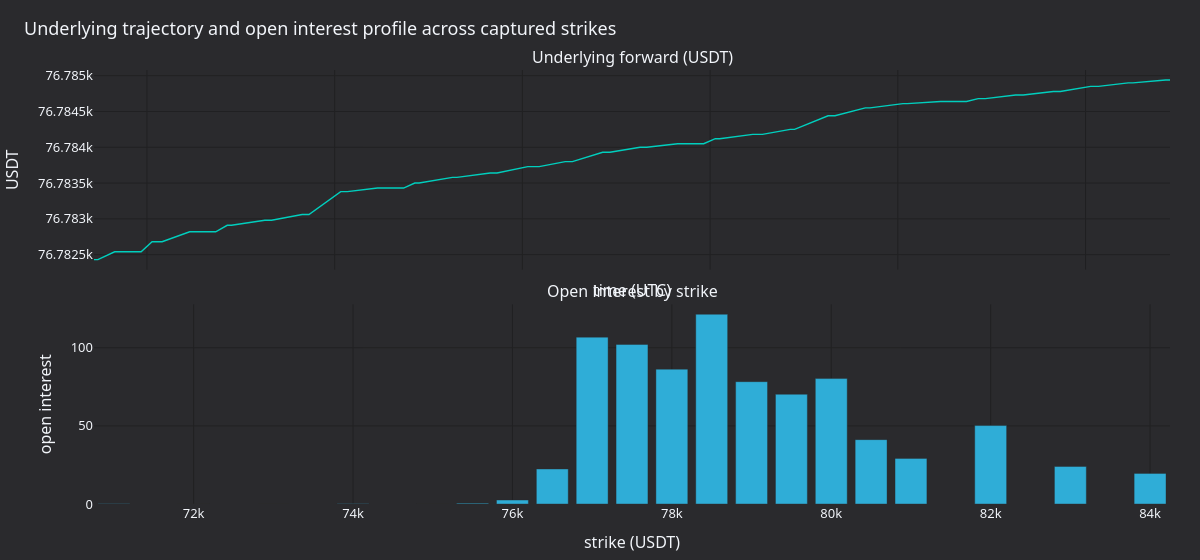

Figure 3. Underlying forward price reported in each Greeks update (top) and open interest by strike at the last update (bottom). OI concentrates in the 70,000-76,000 USDT band: at-the-money to slightly out-of-the-money strikes.

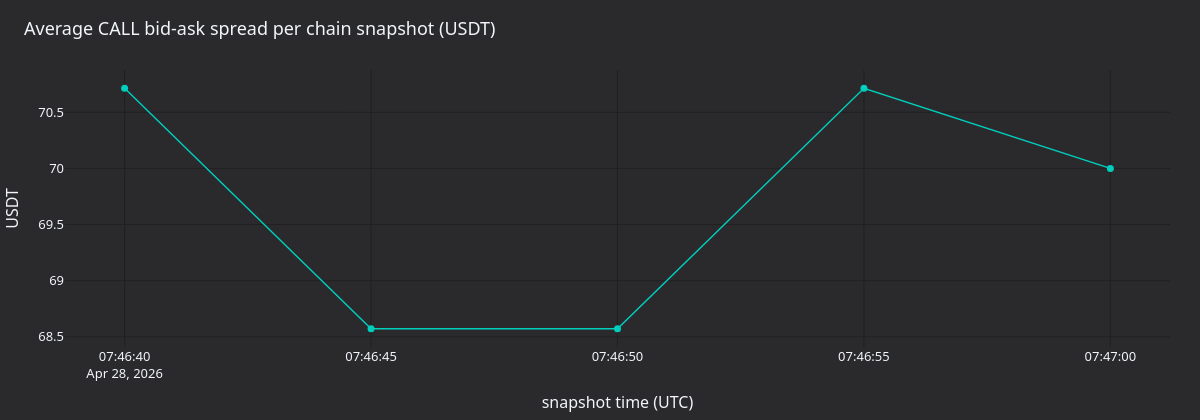

Figure 4. Average CALL bid-ask spread per chain snapshot in USDT.

Snapshots arrive every five seconds (snapshot_interval_ms=5000).

Regenerate the panels

timeout 30 ./target/release/examples/bybit-greeks-tester > /tmp/bybit_greeks.log 2>&1

timeout 30 ./target/release/examples/bybit-option-chain > /tmp/bybit_chain.log 2>&1

uv sync --extra visualization

GREEKS_LOG=/tmp/bybit_greeks.log CHAIN_LOG=/tmp/bybit_chain.log \

python3 docs/tutorials/assets/options_data_bybit/render_panels.pyComplete source

Next steps

- Combine both patterns. Use per-instrument Greeks for near-ATM contracts alongside the aggregated chain view in a single actor. Subscribe to Greeks for contracts you want to track individually, and the chain for a surface-level view.

- Add quote and depth subscriptions. Call

subscribe_quotesfor top-of-bookQuoteTickupdates on individual option contracts. Callsubscribe_order_book_deltaswhen you need the dedicated option orderbook stream. Bybit supports option depths 25 and 100. - Options execution. The

delta-neutral strategy tutorial walks

through a short strangle with perpetual hedging, including IV-based

order placement via Bybit's

order_ivparameter.

See also

- Options: option instrument types, Greeks data types, and chain architecture.

- Bybit integration: full Bybit adapter reference including options order parameters and limitations.

On-Chain Grid Market Making with Short-Term Orders (dYdX)

This tutorial runs the shipped GridMarketMaker strategy on dYdX v4 through the Rust LiveNode. The strategy places symmetric limit orders around the mid...

Delta-Neutral Options Strategy (Bybit)

This tutorial runs a short OTM strangle on Bybit BTC options and delta-hedges with the BTCUSDT perpetual. The strategy selects call and put strikes at...