On-Chain Grid Market Making with Short-Term Orders (dYdX)

This tutorial runs the shipped GridMarketMaker strategy on dYdX v4

through the Rust LiveNode. The strategy places symmetric limit orders

around the mid, skews the grid to manage inventory, and lets the venue

cycle short-term orders by time-to-block expiry instead of explicit

cancels.

Introduction

A grid market maker maintains a ladder of resting buy and sell limits at

fixed price intervals around the current mid. When an order fills, the

strategy profits from the spread between the buy and sell levels.

Inventory management keeps net exposure within max_position so the grid

does not accumulate a directional position.

Inventory skewing (Avellaneda-Stoikov inspired)

When the position grows long the entire grid shifts down (cheaper buys, cheaper sells) to encourage the next fill on the sell side. When the position grows short the grid shifts up. This mirrors the Avellaneda-Stoikov framework adapted to a discrete grid.

Why dYdX v4

dYdX v4 fits market-making well:

- Short-term orders with ~20-second expiry: low-latency placement, no on-chain storage cost.

- ~0.5-second block times for fast confirmation cycles.

- No gas fees for cancellations: short-term cancels are free under GTB replay protection.

- On-chain order book with deterministic per-block matching.

- Batch cancel: one

MsgBatchCancelclears every short-term order.

Prerequisites

Funded dYdX account

You need a dYdX account with USDC collateral. See the Testnet setup section in the integration guide for instructions on creating and funding a testnet account. The testnet wallet also needs an API trading key registered through the dYdX UI.

Environment variables

# Mainnet

export DYDX_PRIVATE_KEY="0x..."

export DYDX_WALLET_ADDRESS="dydx1..."

# Testnet

export DYDX_TESTNET_PRIVATE_KEY="0x..."

export DYDX_TESTNET_WALLET_ADDRESS="dydx1..."Strategy overview

Geometric grid pricing

Each level is a fixed percentage (basis points) away from mid:

Buy level N: mid * (1 - bps/10000)^N - skew

Sell level N: mid * (1 + bps/10000)^N - skewWhere skew = skew_factor * net_position.

For a 3-level grid with grid_step_bps=100 (1%) around a mid of 1000.00:

Sell 3: 1030.30

Sell 2: 1020.10

Sell 1: 1010.00

─── Mid: 1000.00 ───

Buy 1: 990.00

Buy 2: 980.10

Buy 3: 970.30With a long-2 position and skew_factor=1.0, the entire grid shifts down

by 2.0:

Sell 3: 1028.30

Sell 2: 1018.10

Sell 1: 1008.00

─── Mid: 1000.00 ───

Buy 1: 988.00

Buy 2: 978.10

Buy 3: 968.30Inventory management

The strategy enforces position limits through two mechanisms:

max_position: a hard cap on net exposure (long or short). When the projected exposure from adding the next grid level would breach this cap, that level is skipped.- Projected exposure tracking: before placing each level the strategy tracks the worst-case per-side exposure (current position + all pending buy / sell orders) to avoid over-committing.

cancel_all_orders is asynchronous, so pending orders may still fill

between the cancel request and acknowledgement. Tracking worst-case

per-side exposure prevents momentary over-exposure during cancel-requote

transitions.

Requote threshold

requote_threshold_bps controls how much the mid must move before the

strategy cancels all open orders and places a fresh grid:

- Lower threshold (5 bps): more responsive, more cancel/place transactions.

- Higher threshold (50 bps): fewer transactions, but orders may sit further from the current price.

Configuration

| Parameter | Type | Default | Description |

|---|---|---|---|

instrument_id | InstrumentId | required | Instrument to trade (e.g. ETH-USD-PERP.DYDX). |

max_position | Quantity | required | Maximum net exposure (long or short). |

trade_size | Quantity | None | Size per grid level. If None, uses instrument's min_quantity or 1.0. |

num_levels | usize | 3 | Number of buy and sell levels. |

grid_step_bps | u32 | 10 | Grid spacing in basis points (10 = 0.1%). |

skew_factor | f64 | 0.0 | How aggressively to shift the grid based on inventory. |

requote_threshold_bps | u32 | 5 | Minimum mid‑price move in bps before re‑quoting. |

expire_time_secs | Option<u64> | None | Order expiry in seconds. Uses GTD when set, GTC otherwise. |

on_cancel_resubmit | bool | false | Resubmit grid on next quote after an unexpected cancel. |

Choosing parameters

grid_step_bps: 50-100 bps in volatile markets, 5-20 bps in calm conditions. Wider grids capture more spread per fill but fill less often.skew_factor: start at0.0. A value of0.5shifts the grid by 0.5 price units per unit of net position. Too aggressive a skew can move the grid entirely above or below mid.expire_time_secs: for dYdX short-term orders, set to8seconds. That fits inside the 40-block (~20 s) short-term window and keeps the orders on the fast short-term path. WhenNone, orders use GTC and the long-term path.on_cancel_resubmit: triggers a resubmission on the next quote tick after a cancel that the strategy did not initiate (short-term order expiry from the indexer, self-trade prevention, risk limits). The indexer emits a cancel event for each short-term order shortly after it expires; this flag resets the requote anchor so the next quote rebuilds the grid even if the mid has not moved beyondrequote_threshold_bps.

dYdX-specific considerations

Short-term order expiry

When expire_time_secs=8, orders are classified as short-term by the

adapter:

- The adapter checks

8s < max_short_term_secs (40 blocks * ~0.5s = ~20s). - The order is submitted as short-term with

GoodTilBlock = current_height + N. - The order expires on chain after about eight seconds if not filled.

Expiry costs no gas (GTB replay protection handles it on chain), but

the indexer still emits an

OrderCanceledevent for each expired order shortly after the expiry block, so the strategy observes the expiry through the normal cancel event path.

This is the recommended configuration for market making because:

- Short-term orders have lower latency.

- Expiry has no on-chain gas cost.

- Continuous requoting (driven by the indexer-emitted cancel events when

on_cancel_resubmit=true) replaces expired orders.

See the order classification section in the integration guide for full details.

Unexpected cancels and on_cancel_resubmit

The pending_self_cancels set distinguishes self-initiated from

unexpected cancels:

- When the strategy calls

cancel_all_orders, it records all open order IDs inpending_self_cancels. - When

on_order_canceledfires:- If the order ID is in

pending_self_cancels, it is a self-cancel and no action is needed. - Otherwise it was not strategy-initiated (short-term order expiry,

self-trade prevention, or a risk limit). Reset

last_quoted_midso the next quote triggers a full grid resubmission.

- If the order ID is in

This stops the strategy re-quoting unnecessarily during its own cancel waves while still responding to surprises.

on_order_filled also removes the order from pending_self_cancels. If

an order fills before the cancel acknowledgement arrives, this prevents

stale entries from accumulating.

Order quantization

Price and size quantization for dYdX markets is handled automatically by

the adapter's OrderMessageBuilder. No manual rounding or conversion is

needed. See

Price and size quantization

for details.

Post-only orders

All grid orders are submitted with post_only=true. The exchange rejects

any order that would cross the spread at match time, so every fill lands

at the maker fee rate and the grid never inadvertently lifts its own

offers during requote transitions.

Running and stopping

Environment setup

Credentials load from environment variables or a .env file at the

project root (loaded automatically via dotenvy):

# Direct export

export DYDX_PRIVATE_KEY="0x..."

export DYDX_WALLET_ADDRESS="dydx1..."# .env equivalent

DYDX_PRIVATE_KEY=0x...

DYDX_WALLET_ADDRESS=dydx1...Run the example

cargo run --example dydx-grid-mm --package nautilus-dydx --features examplesThe example targets mainnet. To run against testnet, set the DYDX_NETWORK constant near the top

of the example to DydxNetwork::Testnet (this needs a testnet API trading key) and rebuild.

Graceful shutdown

Press Ctrl+C to stop the node. The shutdown sequence:

- SIGINT received, trader stops,

on_stopfires. - Strategy cancels all orders and closes positions.

- 5-second grace period (

delay_post_stop_secs) processes residual events. - Clients disconnect, node exits.

Code walkthrough

The main function lives at

crates/adapters/dydx/examples/node_grid_mm.rs:

const DYDX_NETWORK: DydxNetwork = DydxNetwork::Mainnet;

#[tokio::main]

async fn main() -> Result<(), Box<dyn std::error::Error>> {

dotenvy::dotenv().ok();

let network = DYDX_NETWORK;

let environment = Environment::Live;

let trader_id = TraderId::from("TESTER-001");

let account_id = AccountId::from("DYDX-001");

let node_name = "DYDX-GRID-MM-001".to_string();

let instrument_id = InstrumentId::from("ETH-USD-PERP.DYDX");

let data_config = DydxDataClientConfig {

network,

..Default::default()

};

let exec_config = DydxExecClientConfig {

trader_id,

account_id,

network,

..Default::default()

};

let data_factory = DydxDataClientFactory::new();

let exec_factory = DydxExecutionClientFactory::new();

let log_config = LoggerConfig {

stdout_level: LevelFilter::Info,

..Default::default()

};

let mut node = LiveNode::builder(trader_id, environment)?

.with_name(node_name)

.with_logging(log_config)

.add_data_client(None, Box::new(data_factory), Box::new(data_config))?

.add_exec_client(None, Box::new(exec_factory), Box::new(exec_config))?

.with_reconciliation(false)

.with_delay_post_stop_secs(5)

.build()?;

let config = GridMarketMakerConfig::builder()

.instrument_id(instrument_id)

.max_position(Quantity::from("0.10"))

.num_levels(3)

.grid_step_bps(100)

.skew_factor(0.5)

.requote_threshold_bps(10)

.expire_time_secs(8)

.on_cancel_resubmit(true)

.build();

let strategy = GridMarketMaker::new(config);

node.add_strategy(strategy)?;

node.run().await?;

Ok(())

}Configuration points:

dotenvy::dotenv().ok(): loads.envfrom the project root if present.with_reconciliation(false): disabled for simplicity; enable in production to resume state across restarts.with_delay_post_stop_secs(5): grace period for pending cancel and close events to finalize during shutdown.

Event flow

Strategy internals

The key Rust snippets from grid_mm.rs follow.

Trade size resolution (on_start)

Trade size resolves from the instrument cache: config value first, then

the instrument's min_quantity, then 1.0 as a final fallback.

fn on_start(&mut self) -> anyhow::Result<()> {

let instrument_id = self.config.instrument_id;

let (instrument, size_precision, min_quantity) = {

let cache = self.cache();

let instrument = cache

.instrument(&instrument_id)

.ok_or_else(|| anyhow::anyhow!("Instrument {instrument_id} not found in cache"))?;

(

instrument.clone(),

instrument.size_precision(),

instrument.min_quantity(),

)

};

self.price_precision = Some(instrument.price_precision());

self.instrument = Some(instrument);

if self.trade_size.is_none() {

self.trade_size =

Some(min_quantity.unwrap_or_else(|| Quantity::new(1.0, size_precision)));

}

self.subscribe_quotes(instrument_id, None, None);

Ok(())

}Quote handler (on_quote, abbreviated)

fn on_quote(&mut self, quote: &QuoteTick) -> anyhow::Result<()> {

let mid_f64 = (quote.bid_price.as_f64() + quote.ask_price.as_f64()) / 2.0;

let mid = Price::new(

mid_f64,

self.price_precision

.expect("price_precision should be resolved in on_start"),

);

if !self.should_requote(mid) {

return Ok(()); // Mid hasn't moved enough, keep existing grid

}

self.cancel_all_orders(instrument_id, None, None, None)?;

let (net_position, worst_long, worst_short) = { /* ... */ };

let grid = self.grid_orders(mid, net_position, worst_long, worst_short);

if grid.is_empty() {

return Ok(()); // Don't advance requote anchor when fully constrained

}

let (tif, expire_time) = match self.config.expire_time_secs {

Some(secs) => {

let now_ns = self.clock().timestamp_ns();

let expire_ns = now_ns + secs * 1_000_000_000;

(Some(TimeInForce::Gtd), Some(expire_ns))

}

None => (None, None),

};

for (side, price) in grid {

let order = self.order().limit(

instrument_id,

side,

trade_size,

price,

tif,

expire_time,

Some(true), // post_only

);

self.submit_order(order, None, None)?;

}

self.last_quoted_mid = Some(mid);

Ok(())

}Grid pricing (grid_orders)

Computes geometric grid prices and enforces max_position per level:

fn grid_orders(

&self,

mid: Price,

net_position: f64,

worst_long: Decimal,

worst_short: Decimal,

) -> Vec<(OrderSide, Price)> {

let instrument = self

.instrument

.as_ref()

.expect("instrument should be resolved in on_start");

let mid_f64 = mid.as_f64();

let skew_f64 = self.config.skew_factor * net_position;

let pct = self.config.grid_step_bps as f64 / 10_000.0;

let trade_size = self

.trade_size

.expect("trade_size should be resolved in on_start")

.as_decimal();

let max_pos = self.config.max_position.as_decimal();

let mut projected_long = worst_long;

let mut projected_short = worst_short;

let mut orders = Vec::new();

for level in 1..=self.config.num_levels {

let buy_f64 = mid_f64 * (1.0 - pct).powi(level as i32) - skew_f64;

let sell_f64 = mid_f64 * (1.0 + pct).powi(level as i32) - skew_f64;

let buy_price = instrument.next_bid_price(buy_f64, 0);

let sell_price = instrument.next_ask_price(sell_f64, 0);

if let Some(buy_price) = buy_price

&& projected_long + trade_size <= max_pos

{

orders.push((OrderSide::Buy, buy_price));

projected_long += trade_size;

}

if let Some(sell_price) = sell_price

&& projected_short - trade_size >= -max_pos

{

orders.push((OrderSide::Sell, sell_price));

projected_short -= trade_size;

}

}

orders

}What a 35-second mainnet run produces

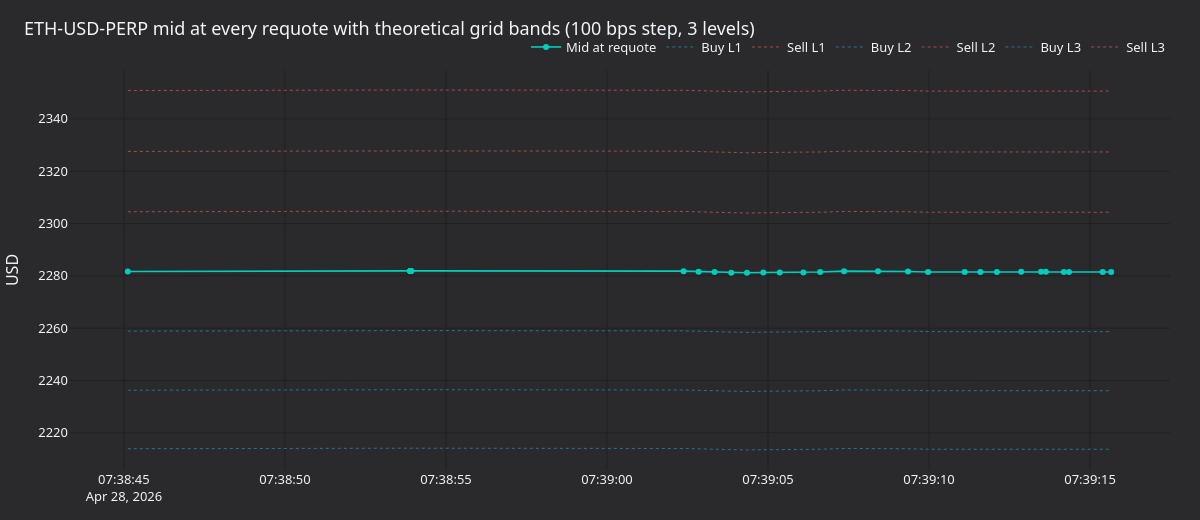

A 35-second mainnet run on ETH-USD-PERP.DYDX with the example config

(grid_step_bps=100, num_levels=3, skew_factor=0.5,

requote_threshold_bps=10, expire_time_secs=8) captures 47 requote

events, 276 order submissions, 67 accepts, and 54 cancels. ETH was

trading near 2,281 USD: the price never moved enough to trip the 10 bps

requote threshold, so most cycles trigger from the periodic 8-second

short-term order expiry rather than from price movement.

Figure 1. ETH-USD-PERP mid at every requote with the six theoretical grid bands (3 levels each side, 100 bps step). Mid sits near 2,281 USD; the inner buy and sell levels are at ~2,258 and ~2,304 USD.

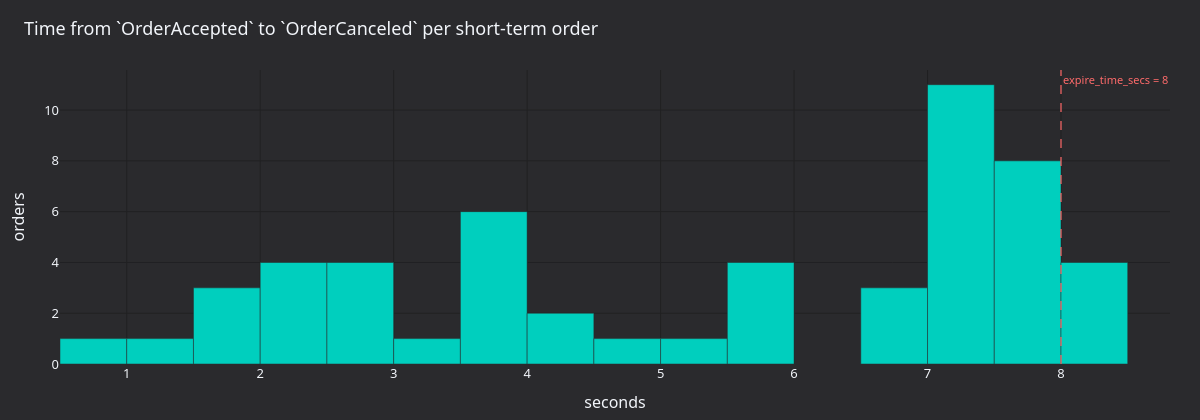

Figure 2. Time from OrderAccepted to OrderCanceled per short-term

order, in seconds. The mass near 7-8 seconds matches the

expire_time_secs=8 setting; the smaller cluster below 6 seconds is

strategy-initiated cancels during requote transitions.

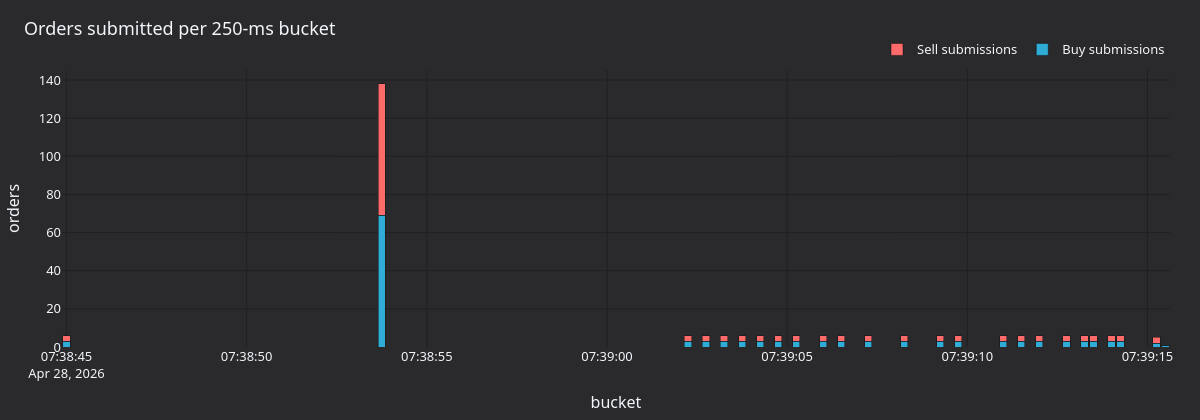

Figure 3. Order submission count per 250-ms bucket, split by side. Each requote cycle places six orders (3 buys + 3 sells); the spacing between bursts is the requote interval.

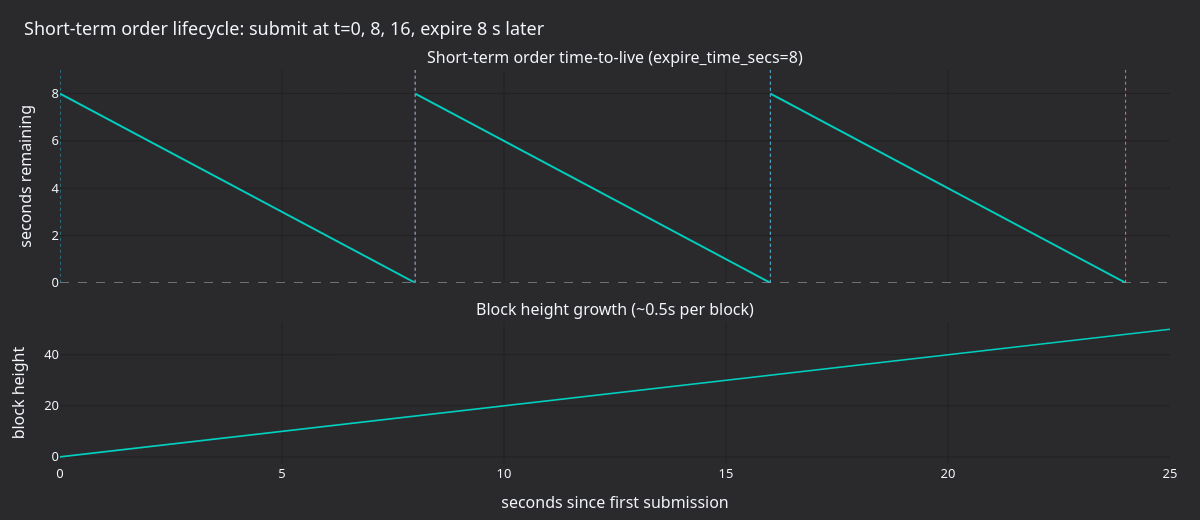

Figure 4. Theoretical short-term order timeline with

expire_time_secs=8 and 0.5-second blocks. The bottom panel tracks how

the chain block height advances; each order's GoodTilBlock target is

set to ~16 blocks ahead, giving the eight-second expiry.

Regenerate the panels

# Capture a 35-second mainnet run.

timeout 35 ./target/release/examples/dydx-grid-mm > /tmp/dydx_main.log 2>&1

uv sync --extra visualization

DYDX_LOG=/tmp/dydx_main.log \

python3 docs/tutorials/assets/grid_market_maker_dydx/render_panels.pyMonitoring and understanding output

Key log messages

| Log message | Meaning |

|---|---|

Requoting grid: mid=X, last_mid=Y | Mid moved beyond threshold, refreshing grid. |

Submit short‑term order N | Order submitted via short‑term broadcast path. |

BatchCancel N short-term orders | Batch cancel executed for expired/stale orders. |

benign cancel error, treating as success | Cancel for an already‑filled or expired order (normal). |

Sequence mismatch detected, will resync and retry | Cosmos SDK sequence error, auto‑recovering. |

Expected behaviour patterns

- Startup: instruments load, WebSocket connects, first quote triggers initial grid.

- Steady state: grid persists across ticks; requotes only when mid

moves more than

requote_threshold_bps. - Fills: position updates, skew adjusts, the next requote shifts the grid.

- Expiry: short-term orders expire on chain after about eight seconds; the indexer emits a cancel event for each, and the next quote refreshes the grid.

- Shutdown: all orders cancelled, positions closed, WebSocket disconnected.

Customization tips

High vs low volatility

| Condition | Adjustment |

|---|---|

| High volatility | Wider grid_step_bps (100-200), fewer num_levels, lower skew_factor. |

| Low volatility | Tighter grid_step_bps (10-30), more num_levels, higher skew_factor. |

| Thin liquidity | Increase requote_threshold_bps to reduce cancel frequency. |

Multiple instruments

Run separate GridMarketMaker instances per instrument. Each instance

manages its own grid, position, and cancel state independently:

let btc_config = GridMarketMakerConfig::builder()

.instrument_id(InstrumentId::from("BTC-USD-PERP.DYDX"))

.max_position(Quantity::from("0.001"))

.base(

StrategyConfig::builder()

.strategy_id(StrategyId::from("GRID_MM-BTC"))

.order_id_tag("BTC".to_string())

.build(),

)

.grid_step_bps(50)

.build();

let eth_config = GridMarketMakerConfig::builder()

.instrument_id(InstrumentId::from("ETH-USD-PERP.DYDX"))

.max_position(Quantity::from("0.10"))

.base(

StrategyConfig::builder()

.strategy_id(StrategyId::from("GRID_MM-ETH"))

.order_id_tag("ETH".to_string())

.build(),

)

.grid_step_bps(100)

.build();

node.add_strategy(GridMarketMaker::new(btc_config))?;

node.add_strategy(GridMarketMaker::new(eth_config))?;Mainnet vs testnet toggle

The example selects the network from the DYDX_NETWORK constant near the top of the file

(DydxNetwork::Mainnet by default). Change it to DydxNetwork::Testnet and rebuild to run

against testnet.

Further reading

- dYdX v4 Integration Guide: full adapter reference.

- dYdX Protocol Documentation: official protocol docs.

- Order types: protocol-level order mechanics.

- Grid Market Making with a Deadman's Switch (BitMEX): comparison with deadman's switch as an alternative to short-term order expiry.

Grid Market Making with a Deadman's Switch (BitMEX)

This tutorial backtests the shipped GridMarketMaker strategy on BitMEX XBTUSD with free historical quote data from Tardis.dev, then runs the same...

Options Data and Greeks (Bybit)

This tutorial connects to Bybit's live options market and consumes Greeks and option chain data through two DataActor examples. It covers instrument...